- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

JPMorgan Chase Goes Against Wall Street: Hoarding Silver, Cornering Gold, Shorting the US Dollar Credit

Original Article Title: "JPMorgan Turns Against Wall Street: Hoarding Silver, Stashing Gold, Shorting the Dollar"

Original Article Author: sleepy.txt, Watcher Beating

JPMorgan Chase, the most loyal "gatekeeper" of the old US Dollar order, is now actively tearing down the very walls it once swore to defend.

According to market rumors, by the end of November 2025, JPMorgan Chase will relocate its core precious metals trading team to Singapore. If the geographical migration is merely a surface-level change, its core signifies a public defection from the Western financial power structure.

Looking back over the past half-century, Wall Street has been responsible for constructing a vast credit illusion based on the US Dollar, while London, as the "heart" of Wall Street's financial empire across the Atlantic, has maintained pricing integrity with deep underground vaults. Together, they have interwoven a tight control grid over the Western world's precious metals. JPMorgan Chase, supposed to be the ultimate and most robust line of defense, was part of this system.

The writing was on the wall, the signs were there. Amid official silence on the rumors, JPMorgan Chase executed a stunning asset maneuver, discreetly reclassifying around 169 million troy ounces of silver from the "Eligible" category in the COMEX vault to the "Registered" category. Roughly estimated based on LBMA public data, this amount is equivalent to nearly 10% of the global annual supply, now locked away on the balance sheet.

In the ruthless game of commerce, scale itself is a display of the most unyielding attitude. To many traders, this mountainous hoard of over 5,000 tons of silver appears more like a strategic reserve set aside by JPMorgan Chase as a bargaining chip for the next pricing power struggle.

Simultaneously, thousands of kilometers away, Singapore's largest private vault, The Reserve, coincidentally initiated its Phase Two expansion, increasing the vault's total capacity to a level of 15,500 tons in one go. This infrastructure upgrade, planned five years ago, has provided Singapore with enough confidence to absorb the massive wealth overflowing from the West.

JPMorgan Chase locks down physical liquidity in the West to create panic with one hand, while it builds a sheltered reservoir in the East to reap the rewards with the other.

What prompted this titan to turn against its own kind was the undeniable fragility of the London market. At the Bank of England, the delivery timeline for gold stretched from days to weeks, while the silver lease rates skyrocketed to 30%, hitting historic highs. To those familiar with this market, this at least signals one thing: everyone is scrambling for supply, and the physical assets in the vaults are starting to run dry.

The most astute market players are often also the vultures with the keenest sense of the scent of death.

In this harsh winter, JPMorgan Chase has showcased the impeccable instinct of a top-tier banker. Its exit marks the end of a half-century-long, alchemical game of "paper gold" that is now drawing to a close. As the tide recedes, only those holding onto the heavy, tangible chips will secure a ticket to the next thirty years.

The Alchemy's End

The root of all calamity was sown half a century ago.

In 1971, when President Nixon severed the tie between the US dollar and gold, he effectively unplugged the last anchor of the global financial system. From that moment on, gold transitioned from a rigidly redeemable currency to a financial asset redefined by Wall Street.

Over the subsequent half-century, bankers in London and New York concocted a sophisticated form of "financial alchemy." Since gold was no longer a currency, it could be conjured out of thin air in countless "contracts" akin to printing money.

This gave rise to the massive derivatives empires established by the LBMA (London Bullion Market Association) and COMEX (Commodity Exchange Inc.). In this empire, leverage reigns supreme. For every slumbering gold bar in the vault, there exist 100 churned-out delivery slips in the market. And on the silver gaming tables, this play is even more frenzied.

This system of "paper affluence" has sustained itself for half a century, entirely reliant on a fragile gentleman's agreement: the vast majority of investors are merely seeking to profit from spreads and should never attempt to claim that heavy piece of metal.

However, the architects of this game failed to anticipate the charging "grey rhino" bursting into the room—silver.

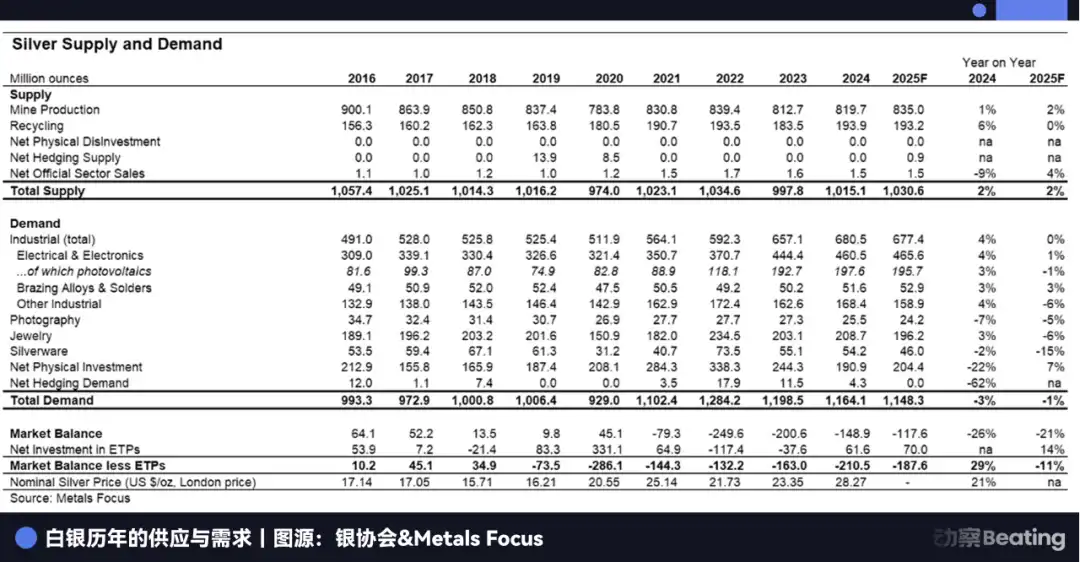

Unlike gold, which lies as eternal wealth deep underground, silver plays the role of a "commodity" in the modern industry. It's the lifeblood of solar panels and the nerve of electric vehicles. According to data from the Silver Institute, the global silver market has faced a structural deficit for five consecutive years, with industrial demand representing nearly sixty percent of total demand.

While Wall Street can type infinite dollars on a keyboard, it cannot create an ounce of conductive silver out of nothing.

As physical inventories are devoured by the real economy, the paper millions of contracts become worthless. By this winter of 2025, the thin veil has finally been pierced.

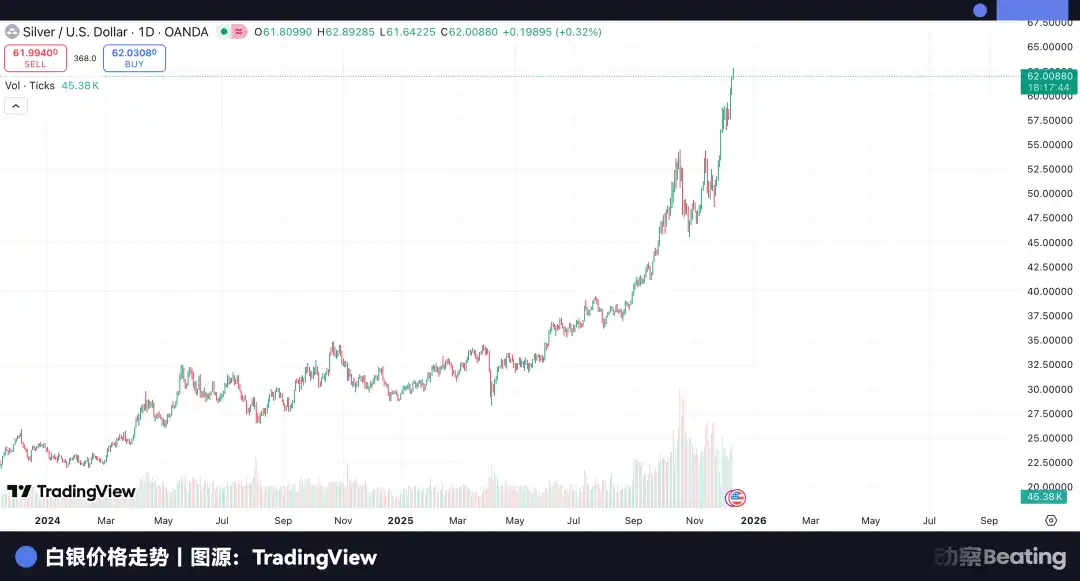

The first warning sign was the price anomaly. In the normal futures logic, forward prices are typically higher than spot prices, known as "backwardation." Yet in London and New York, the markets experienced an extreme form of "spot premium." If you wanted to buy a silver contract for delivery six months from now, all was peaceful; but if you aimed to take the silver bar home right now, not only would you face a hefty premium, but also endure weeks of protracted waiting.

A long line formed outside the Bank of England's vault, COMEX's registered silver inventory fell below the safety red line, and the open interest to physical inventory ratio briefly soared to 244%. The market finally understood the terrifying reality: physical assets and paper contracts were splitting into two parallel universes. The former belonged to those who owned factories and vaults, while the latter belonged to speculators still lost in old dreams.

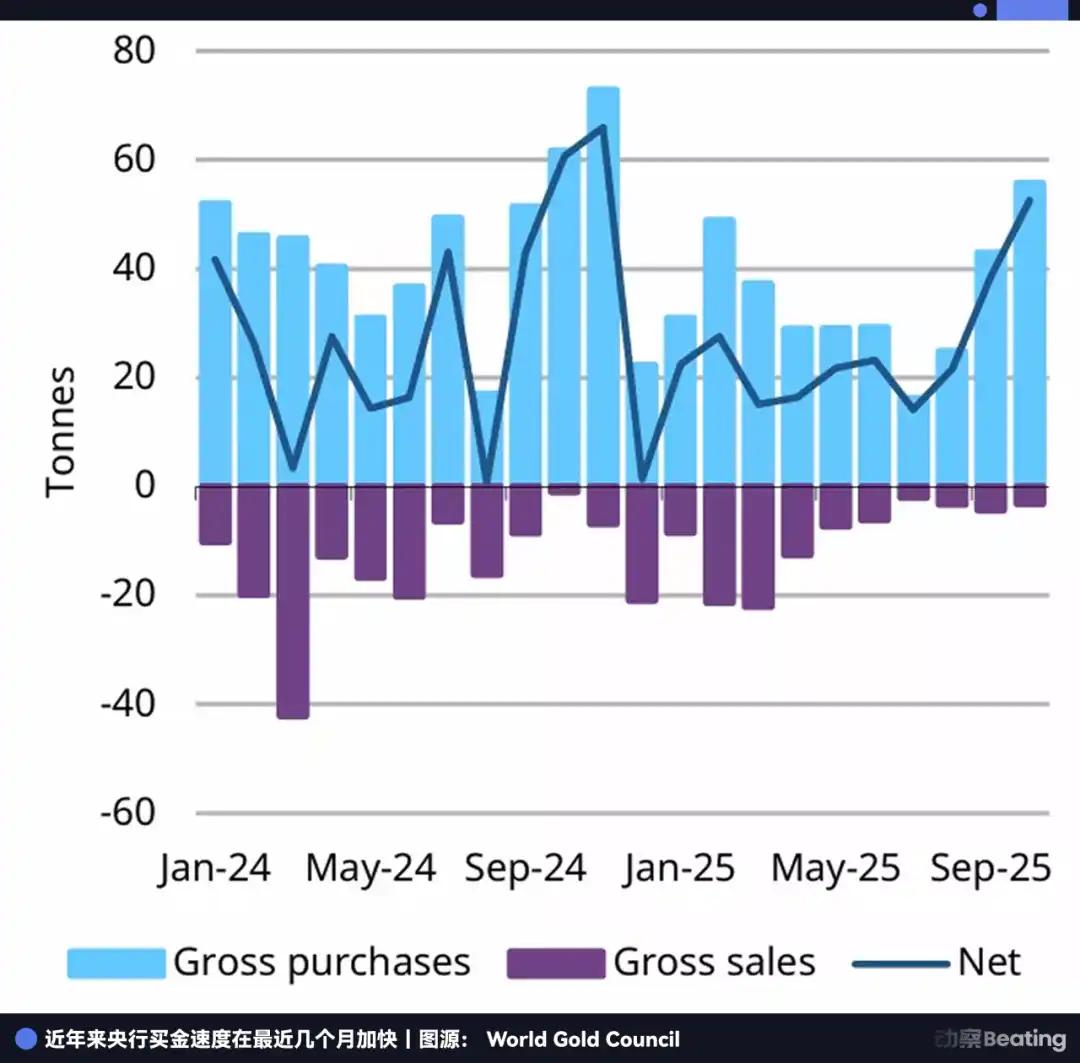

If silver's scarcity was due to the devouring of the industrial behemoth, then gold's disappearance was the result of a national-level "run." Central banks around the world, once the most steadfast holders of the US dollar, were now at the forefront of the run.

Despite gold's price being at a historic high in 2025, causing some central banks to tactically slow down their gold purchases, "buying" remained the only strategic move. The World Gold Council's (WGC) latest data showed that in the first 10 months of 2025, global central banks cumulatively purchased a net total of 254 tons of gold.

Let's take a look at this buyer's list.

Poland, after pausing gold purchases for 5 months, made a sudden comeback in October, sweeping up 16 tons in a single month, forcibly raising its gold reserve ratio to 26%. Brazil increased its holdings for two consecutive months, reaching a total of 161 tons. China, since resuming purchases in November 2024, has appeared on the buyer's list for the 13th consecutive month.

These countries spared no effort to exchange precious foreign exchange for heavy gold bars to be shipped back to their homelands. In the past, everyone trusted US Treasuries because they were considered "risk-free assets"; now, everyone was scrambling for gold because it had become the sole shield against "dollar credit risk."

Although mainstream Western economists are still arguing, claiming that the paper gold system provides efficient liquidity and that the current crisis is only a temporary logistics issue.

But paper cannot contain a fire, and now it cannot contain gold.

When the leverage ratio reaches 100:1, and that sole "1" begins to be resolutely taken back home by central banks worldwide, the remaining "99" paper contracts face an unprecedented liquidity mismatch.

The current London market is falling into a typical short squeeze dilemma, with industrial giants busy grabbing silver to ensure production continuity, while central banks are firmly holding onto gold as a national fate reserve. When all trading counterparties are demanding physical delivery, pricing models based on credit foundations fail. Whoever holds the physical asset holds the power to define the price.

And JPMorgan Chase, the "grand magician" who was once most adept at playing with paper contracts, clearly saw this future earlier than anyone else.

Instead of being a foot soldier of the old order, it would rather be a partner of the new order. This habitual offender, fined $920 million for market manipulation over the past eight years, did not leave out of a sudden attack of conscience, but rather made a precise bet on the global wealth redistribution over the next thirty years.

What it bet on was the collapse of the "paper contract" market. Even if the collapse is not immediate, that layer of infinitely leveraged positions will sooner or later be cut off round after round. The only truly safe asset left is the visible and touchable metal in the warehouse.

Wall Street Betrayal

If the paper gold and silver system is likened to a flashy casino, then in the past decade, J.P. Morgan was not only the security guard maintaining order but also the dealer most skilled at cheating.

In September 2020, to settle the U.S. Department of Justice's charges of manipulating the precious metals market, J.P. Morgan paid a record $920 million in fines. In the thousands of pages of investigation documents disclosed by the Justice Department, J.P. Morgan's traders were depicted as masters of deceptive tactics.

They were adept at a very cunning hunting technique. Traders would instantly place thousands of contracts on the sell side, creating the illusion of an imminent price collapse, inducing retail and high-frequency robots to panic sell; then, at the moment of the collapse, they would cancel their orders and turn around to gorge on the blood-soaked chips at the bottom.

According to statistics, J.P. Morgan's former global head of precious metals, Michael Nowak, and his team artificially created momentary price collapses and surges in the price of gold and silver tens of thousands of times over an eight-year period.

At that time, the outside world generally attributed all this to Wall Street's usual greed. But five years later today, when that jigsaw puzzle of 169 million ounces of silver inventory is laid out on the table, a darker idea begins to circulate in the market.

In some people's interpretation, J.P. Morgan's "manipulation" at that time is hard to be seen merely as trying to earn a little more from high-frequency trading spreads. It looks more like a slow and prolonged chip-siphoning, with them violently pressing down prices on the paper market to create the illusion of a held-down price; while quietly gathering chips on the physical side.

This former guardian of the old order of the dollar has now transformed into the most dangerous gravedigger of the old order.

In the past, J.P. Morgan was the largest short seller in paper silver, the ceiling suppressor of gold and silver prices. But now, with the physical chips fully swapped, overnight they have become the largest long position.

Market gossip has never been scarce. There are rumors that the recent surge in the silver price from $30 to $60 was orchestrated behind the scenes by J.P. Morgan itself. While such claims lack evidence, they are enough to illustrate one thing - in many people's minds, it has transitioned from a manipulator shorting paper silver to the biggest long position in physical assets.

If all this deduction holds true, then we will witness the most spectacular and ruthless mutiny in commercial history.

JPMorgan understands better than anyone else that the iron fist of U.S. regulation is tightening inch by inch, and the game of paper contracts, which may demand not only money but even lives, has reached its end.

This also explains why it has such a fondness for Singapore.

In the U.S., every transaction can be flagged as suspicious by an AI surveillance system; but in Singapore, within those private fortresses not belonging to any national central bank, gold and silver are completely depoliticized. There is no extraterritorial jurisdiction here, only utmost protection of private property.

JPMorgan's breakout is by no means a solo effort.

Right at the same time when rumors were fermenting, the top consensus on Wall Street had quietly been reached. Although there was no physical collective relocation, strategically, the giants had accomplished an astonishing synchronized shift. Goldman Sachs set its 2026 gold price target aggressively at $4,900, and Bank of America even boldly proclaimed a sky-high $5,000.

In the era dominated by paper gold, such price targets sound like a pipe dream; but if we shift our focus back to physical assets, observing the central banks' gold buying pace and the inventory changes in the vaults, this number begins to have room for serious discussion.

The smart money on Wall Street is quietly reallocating, reducing some gold shorts and increasing physical positions, not necessarily dumping all U.S. treasuries, but slowly adding gold, silver, and other physical assets to the portfolio. JPMorgan's move is the fastest, the boldest, because it not only wants to survive but also to win. It doesn't want to go down with the paper gold empire; it wants to take its algorithms, capital, and technology to a place that not only has gold but also has a future.

The issue is that that place already has its own master.

As JPMorgan's private jet lands at Singapore Changi Airport, looking north, it will find a larger opponent that has long built high walls there.

The Surging Waves

While London traders are still fretting over the liquidity drought of paper gold, thousands of kilometers away on the banks of the Huangpu River in Shanghai, a vast empire of physical gold has already completed its original accumulation.

Its name is the Shanghai Gold Exchange (SGE).

In the Western-dominated financial landscape, the SGE is a complete outlier. It rejects the virtual game built on credit contracts seen in London and New York and, from its inception, has staunchly upheld an almost paranoid rule: physical delivery.

These four words, like a steel nail, were precisely driven into the heart of the Western paper gold game.

At the New York COMEX, gold is often just a series of fluctuating numbers, with the majority of contracts being liquidated before expiration. But in Shanghai, the rules are "full-amount trading" and "centralized clearing."

Behind every transaction here, there must be a real gold bar lying in the vault. This not only eliminates the possibility of unlimited leverage but also raises the bar for "shorting gold" because you must first borrow real gold before you can sell it.

In 2024, the SGE delivered an astonishing report card, with the annual gold trading volume reaching 62.3 thousand tons, a 49.9% increase from 2023; transaction value soared to 34.65 million yuan, an increase of nearly 87%.

While the physical delivery rate of the New York COMEX is less than 0.1%, the Shanghai Gold Exchange has become the world's largest physical gold reservoir, continuously absorbing global bullion.

If the inflow of gold is a country's strategic reserve, then the inflow of silver is the "physiological desire" of China's industry.

Wall Street speculators can use paper contracts to bet on prices, but as the world's largest base for solar and new energy manufacturing, Chinese factory owners don't want contracts; they must have real silver to start production. This rigid industrial demand has made China the world's largest precious metals black hole, constantly devouring Western stocks.

The path of "Western Gold Moving East" is busy yet secretive.

Take the journey of a gold bar, for example. In the Swiss canton of Ticino, the world's largest gold refineries (such as Valcambi, PAMP) are operating around the clock. They are carrying out a special "blood exchange" task, melting down 400-ounce standard gold bars brought from the London vaults, refining them, then recasting them into 1 kg, 99.99% pure "Shanghai Gold" standard bars.

This is not just a physical recasting but also a transformation of monetary attributes.

Once these gold bars are melted into 1 kg specifications and stamped with "Shanghai Gold," they are almost impossible to flow back to the London market. Because to return, they must be melted and re-certified, incurring extremely high costs.

This means that once gold flows eastward, it is like a river flowing into the sea, never to return. The surging waves flow on, thousands of miles of rivers and never-ending tides.

On the tarmac of major airports around the world, armored caravans bearing the insignia of Brink's, Loomis, or Malca-Amit are the movers of this great migration. They have continuously filled Shanghai's vaults with these recast gold bars, becoming the physical cornerstone of the new order.

Mastering the physical means mastering the discourse. This is the strategic significance that SGE Chairman Yu Wenjian has repeatedly emphasized in establishing the "Shanghai Gold" benchmark price.

For a long time, global gold pricing power has been firmly locked in the London PM Gold Fix, as it embodies the will of the US dollar. However, Shanghai is attempting to sever this logic.

This is a high-dimensional strategic hedge. As China, Russia, the Middle East, and other countries begin to form an invisible alliance for "de-dollarization," they need a new common language. This language is not the Renminbi, nor the Ruble, but gold.

Shanghai is the translation center for this new language. It is telling the world that if the dollar is no longer trustworthy, then please believe in the real gold and silver stored in your own warehouse; if paper contracts may default, then please believe in Shanghai's rule of payment upon delivery.

For J.P. Morgan Chase, this is both a massive threat and an undeniable opportunity.

To the West, there is no turning back, as there is only depleted liquidity and tightened regulation; to the East, it must confront the behemoth that is Shanghai. It cannot directly conquer Shanghai because the rules there do not belong to Wall Street, and the walls there are too thick.

The Final Buffer Zone

If Shanghai is the "heart" of the Eastern physical asset empire, then Singapore is the "frontline" of this East-West showdown. It is not just a geographical transit point but also the carefully chosen last line of defense for Western capital in the face of the rise of the East.

Singapore, this city-state, is investing almost frantically to transform itself into the "Switzerland" of the 21st century.

Le Freeport, located next to the Changi Airport runway, is the best window to observe Singapore's ambition. This free port, with independent judicial status, is a perfect "black box" both in physical and legal terms. Here, the movement of gold is stripped of all cumbersome administrative oversight, and the entire process from the plane landing to the gold bars being stored is completed within a completely closed, tax-free, and highly private loop.

At the same time, another super vault named The Reserve has been on high alert since 2024. This 180,000-square-foot fortress has a total design capacity of up to 15,500 tons. Its selling point is not only the one-meter-thick reinforced concrete walls but also a privilege bestowed by the Singapore government—full exemption from Goods and Services Tax (GST) for Investment Precious Metals (IPM).

For a market maker like JPMorgan, this is an irresistible temptation.

But if it's solely for tax reasons and a vault, JPMorgan could easily choose Dubai or Zurich. It ultimately chose Singapore, with deeper geopolitical calculations at play.

On Wall Street, directly moving the core business from New York to Shanghai is akin to "defecting," which is tantamount to suicide in the current murky waters of international politics. They urgently need a fulcrum, a place that can not only access the vast physical market in the East but also provide them with a politically secure haven.

Singapore is precisely the only choice.

It guards the Strait of Malacca, connecting London's dollar liquidity while reaching Shanghai and India's physical demand.

Singapore is not only a safe haven but also the biggest hub connecting two divergent worlds. JPMorgan is trying to establish a round-the-clock trading loop here: benchmarking in London, hedging in New York, and stocking up in Singapore.

However, JPMorgan's ideal scenario is not without its flaws. In the battle for pricing power in Asia, it cannot bypass its strongest competitor—Hong Kong, China.

Many mistakenly believe that Hong Kong has fallen behind in this competition, but the opposite is true. Hong Kong, China possesses a key card that Singapore cannot replicate: it is the sole channel for the offshore renminbi.

Through the "Gold Connect," the Chinese Gold & Silver Exchange (CGSE) in Hong Kong is directly linked to the Shanghai Gold Exchange. This means that gold traded in Hong Kong can directly enter the delivery system in mainland China. For those truly looking to embrace the Chinese market, Chinese Hong Kong is not "offshore" but an extension of the "onshore."

JPMorgan chose Singapore, betting on a hybrid model of "dollar + physical," attempting to establish a new offshore center on the ruins of the old order. Meanwhile, traditional British banks like HSBC and Standard Chartered continue to heavily invest in Hong Kong, betting on the "renminbi + physical" future.

JPMorgan believed it had found a neutral safe haven, but in the geopolitical meat grinder, there was never a true "middle ground." The prosperity of Singapore is fundamentally the result of the overflow of the Eastern economy. This seemingly independent luxury yacht has long been locked into the gravitational field of the Eastern mainland.

As Shanghai's gravitational force grows stronger, as the realm of renminbi-denominated gold expands, as China's industrial machine continues to devour physical silver in the market, Singapore may no longer be a neutral safe haven, and JPMorgan will once again have to make a fateful decision.

Restart of the Cycle

Regarding the rumors about J.P. Morgan, there may eventually be an official explanation, but that is no longer important. In the world of business, astute capital always perceives seismic activity at the first moment.

The epicenter of this tremor is not in Singapore, but in the depths of the global monetary system.

For the past fifty years, we have been accustomed to a "paper contract" world dominated by dollar credit. It was an era built on debt, commitments, and the illusion of infinite liquidity. We once thought that as long as the printing press was running, prosperity could be sustained.

But now, the wind has completely changed.

As central banks around the world spare no effort to repatriate gold, and as global manufacturing giants begin to anxiously vie for the last piece of industrial silver, what we see is a return to an ancient order.

The world is slowly but surely moving from an elusive credit monetary system back to a tangible asset-based system. In this new system, gold is the measure of credit, and silver is the measure of productive capacity. One represents the secure bottom line, and the other represents the industrial limit.

In this long migration, London and New York are no longer the sole destinations, and the East is no longer just a mere factory. New rules of the game are being formulated, and new centers of power are taking shape.

The era defined by Western bankers as the value of gold and silver is slowly fading away. Gold and silver remain silent, yet they answer all questions about the era.

You may also like

From 0 to $1 Million: Five Steps to Outperform the Market Through Wallet Tracking

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

From 0 to $1 Million: Five Steps to Outperform the Market Through Wallet Tracking

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.