- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

How do 8 Top Investment Banks View 2026? Gemini Read Through for You and Highlighted the Key Points

Original Title: Bank Outlooks 2026 Research Plan

Original Author: szj capital

Original Translator: Deep Tide TechFlow

As the year comes to a close, major institutions have begun to forecast the market for the coming year.

Recently, overseas netizens have compiled the annual outlook reports of 8 top investment banks including Goldman Sachs, BlackRock, Barclays, and HSBC, allowing Gemini Pro3 to conduct a comprehensive interpretation and analysis.

The following is a full translation to help you save time and get an overview of next year's key economic trends.

Executive Summary: Embracing the "K-Shaped" New World Order

2026 is destined to be a period of profound structural transformation, characterized not by a singular synchronized global cycle, but by a complex and diverse economic reality intertwined with policy dissonance and thematic disruption. This comprehensive research report brings together forward-looking strategies and economic forecasts from leading global financial institutions, including J.P. Morgan Asset Management, BlackRock, HSBC Global Private Banking, Barclays Private Bank, BNP Paribas Asset Management, Invesco, T. Rowe Price, and Allianz.

These institutions collectively paint a picture of a "bend but not break" global economic landscape: the past decade's "easy money" era has been replaced by a new paradigm of "Higher for Longer" interest rates, Fiscal Dominance, and Technological Disruption. The core theme of 2026, as identified by Barclays Private Bank, is "The Interpretation Game," an environment of conflicting economic data and rapidly changing narratives where market participants must actively interpret conflicting signals rather than rely on passive investment.

One of the key pillars of 2026 is the significant divergence between the United States and other countries. J.P. Morgan and T. Rowe Price believe that the U.S. economy is being driven by AI capital expenditures and a fiscal stimulus known as the "One Big Beautiful Bill Act (OBBBA)," creating a unique growth dynamic. This stimulus is expected to bring an "excitement effect" of over 3% in early 2026, gradually tapering off thereafter; while Allianz and BNP Paribas expect the Eurozone to exhibit a "flat is the new beautiful" mode of recovery.

However, beneath the surface growth numbers lies a more turbulent reality. Allianz has warned that the global corporate bankruptcy rate will hit a "historic high," with a projected 5% increase by 2026, representing the final blow to "zombie firms" from the high-rate hangover effect. This scenario outlines a "K-shaped" expansion where large-cap tech companies and infrastructure sectors thrive due to the "AI Mega Force" (BlackRock concept), while leverage-dependent small businesses face a survival crisis.

Asset allocation consensus is undergoing a significant shift. The traditional 60/40 investment portfolio (60% stocks, 40% bonds) is being redefined. BlackRock has introduced the concept of the "New Continuum," suggesting that the boundaries between public and private markets are blurring, and investors need to permanently allocate to private credit and infrastructure assets. Schroders and HSBC recommend a return to "quality" in fixed income investments, favoring investment-grade bonds and emerging market debt while shunning high-yield bonds.

This report systematically analyzes each institution's investment themes, covering "Physical AI" trading, the "Electrotech Economy," the rise of protectionism and tariffs, and the strategic focuses investors should take in this fractured world.

Part 1: Macroeconomic Landscape — A Multi-Speed Growth World

In the post-pandemic era, the anticipated synchronized global recovery has not materialized. 2026 presents a landscape characterized by unique growth drivers and policy differentiations. Major economies are progressing at varying speeds due to their fiscal, political, and structural forces.

1.1 United States: The "North Star" of the Global Economy and the OBBBA Stimulus

The United States remains the undisputed engine of the global economy, but its growth dynamics are shifting. It is no longer solely reliant on organic consumer demand but increasingly on government fiscal policy and corporate capital expenditure in artificial intelligence.

The Phenomenon of the "One Big Beautiful Bill Act" (OBBBA)

A key finding in Morgan Stanley Investment Management and PIMCO's 2026 outlook is the anticipated impact of the "One Big Beautiful Bill Act" (OBBBA). This legislative framework is seen as the defining fiscal event of 2026.

· Operation Mechanism: Morgan Stanley highlights that the OBBBA is a comprehensive legislative package that extends key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) while introducing new spending items. It includes around $170 billion for border security (law enforcement, deportation) and $150 billion for defense spending (such as the "Golden Dome" missile defense system and shipbuilding). Additionally, the bill raises the debt ceiling by $5 trillion, indicating that loose fiscal policy will continue.

· Economic Impact: PwC Group believes that this bill, combined with AI spending, will help the U.S. economy break free from growth anxiety by the end of 2025. JPMorgan Chase predicts that OBBBA will drive real GDP growth to around 1% in the fourth quarter of 2025 and accelerate to over 3% in the first half of 2026 as tax refunds and spending flow directly into the economy. However, this growth is seen as a temporary surge — a reversal of the "fiscal cliff" — as growth is expected to taper off to a 1-2% trend line in the second half of the year.

· Tax Impact: The bill is expected to permanently extend the 37% top individual income tax rate and restore 100% bonus depreciation for businesses and R&D expense deductions. Morgan Stanley highlights that this is a significant supply-side incentive that could lower the effective corporate tax rate in certain industries to as low as 12%, driving a "Capex Supercycle" in manufacturing and technology sectors.

The Labor Market Paradox: "Economic Drift"

Despite fiscal stimulus, the U.S. economy continues to face a major structural impediment: labor supply. JPMorgan Chase describes this environment as "Economic Drift," noting that a sharp decline in net immigration is expected to result in an absolute decrease in the working-age population.

· Impact on Growth: This supply constraint implies that only 50,000 new jobs are expected to be added per month in 2026. This is not a failure of demand but a bottleneck on the supply side.

· Unemployment Rate Ceiling: Therefore, the unemployment rate is expected to remain at a low level, peaking at 4.5%. This "full employment" dynamic, while preventing a deep recession, also sets a hard limit on potential GDP growth, further exacerbating the sense of economic "drift" — despite positive data, the economy appears to be stagnating.

1.2 Eurozone: The Surprising Nature of "Flat is Beautiful"

In stark contrast to the U.S. narrative full of volatility and fiscal drama, the Eurozone is gradually becoming a symbol of stability. Allianz and BNP Paribas believe that Europe may outperform expectations and excel in 2026.

Germany's "Fiscal Reset"

BNP Paribas points out that Germany is undergoing a critical structural transformation. Germany is gradually moving away from its traditional "black zero" fiscal austerity policy and is expected to significantly increase spending in infrastructure and defense. This fiscal expansion is expected to have a multiplier effect across the entire Eurozone, boosting economic activity levels in 2026.

Consumer Support Policy

In addition, BNP Paribas mentioned that permanent measures such as the reduced VAT for the restaurant industry and energy subsidies would support consumer spending, thereby avoiding a demand collapse.

Growth Forecast

Allianz forecasts that the Eurozone's GDP growth rate in 2026 will be between 1.2% and 1.5%. While this number may seem modest compared to the US's "OBBBA stimulus," it represents a robust and sustainable recovery from the stagnation of 2023-2025. Barclays also shares a similar view, believing that the Eurozone may bring "positive surprises."

1.3 Asia and Emerging Markets: "Extended Runway" and Structural Slowdown

The outlook for Asia shows a clear dichotomy: on one hand, there is a gradually maturing China with slowing growth, and on the other hand, there is the dynamic and rapidly growing India and ASEAN region.

China: Orderly Deceleration

Major institutions generally agree that China's era of high-speed growth has ended.

· Structural Resistance: BNP Paribas forecasts that by the end of 2027, China's economic growth rate will slow to below 4%. PwC Group adds that despite stimulus measures, due to deep-rooted issues in the real estate market and population structure, these measures are unlikely to bring about a "substantial boost."

· Targeted Stimulus: Different from a comprehensive "all-out" stimulus, the Chinese government is expected to focus on supporting the "advanced manufacturing" and strategic industries. This shift aims to move the economy upstream in the value chain but will sacrifice short-term consumption growth. Barclays predicts that China's consumption growth in 2026 will be only 2.2%.

India and ASEAN: Growth Engines

In contrast, HSBC and S&P Global believe that South Asia and Southeast Asia are becoming the new global growth champions.

· India's Growth Trajectory: HSBC expects India's GDP growth rate in 2026 to be 6.3%, making it one of the fastest-growing major economies. However, HSBC also issues a tactical warning: despite strong macroeconomic performance, there may be a relative weakness in short-term corporate earnings growth, potentially creating a disconnect with high valuations that could affect equity investors.

· Artificial Intelligence in the Supply Chain: Both J.P. Morgan and HSBC emphasize the significant role of the "Artificial Intelligence theme" in driving Asia's emerging markets, especially in Taiwan and South Korea (semiconductor sector) and ASEAN countries (data center assembly and component manufacturing). The "expansion" of artificial intelligence trade is a key driver in the region.

1.4 Global Trade: The "Tariff Tax Effect"

In the 2026 outlook, a potential shadow is the resurgence of protectionism. HSBC has clearly lowered its global growth expectations from 2.5% to 2.3%, mainly due to the United States' initiation of "omnibus tariffs."

Stagnation in Trade Growth

HSBC predicts that global trade growth in 2026 will be only 0.6%. This near-stagnant state reflects a world where supply chains are shortening ("nearshore outsourcing") and realigning to circumvent tariff barriers.

Inflation Pressure

S&P Global warns that these tariffs will act as consumption taxes, leading to sustained inflation in the United States "above target levels."

Part Two: The Conundrum of Inflation and Interest Rates

The era of the "Great Moderation" prior to the 2020s has been replaced by a new normal of volatility. Stubborn inflation in the United States intertwined with deflationary pressures in Europe has driven a "Great Decoupling" of central bank policies.

2.1 Divergence in Inflation

· United States: Stubborn and Structural

S&P Global and BNP Paribas see high inflation persisting in the United States due to OBBBA fiscal stimuli and tariff impacts. J.P. Morgan provides a more detailed analysis, expecting inflation to peak near 4% in the first half of 2026 due to tariff increases but to recede to 2% by year-end as the economy gradually absorbs the shock.

· Europe: Deflationary Surprise

In contrast, BNP Paribas notes that Europe faces deflationary pressures, partly due to the re-circulation of "cheap Chinese export goods" entering the European market. This may lead to inflation below the European Central Bank's (ECB) target, contrasting sharply with the inflation trend in the United States.

2.2 Decoupling of Central Bank Policies

The divergence in inflation dynamics has directly led to a split in monetary policies, creating opportunities for macro investors.

· Federal Reserve ("Gradual" Path)

The Federal Reserve is expected to be constrained. J.P. Morgan anticipates that the Fed may only cut rates 2-3 times by 2026. On the other hand, PIMCO is more hawkish, warning that if the OBBBA fiscal stimulus leads to overheating, the Fed may not be able to cut rates at all in the first half of 2026.

· European Central Bank ("Dovish" Path)

Facing weak growth prospects and deflationary pressures, the European Central Bank is expected to make significant rate cuts. Allianz and BNP Paribas predict that the ECB will lower rates to 1.5%-2.0%, well below current market expectations.

· Impact on the Foreign Exchange Market

This widening interest rate differential (with U.S. rates remaining high and Eurozone rates falling) implies a structural strength of the U.S. dollar against the euro, contrary to the consensus that the dollar weakens during economic cycles maturity. However, Invesco holds the opposite view, betting that a weaker dollar will support emerging market assets.

Part Three: In-Depth Analysis of Themes - "Mega Forces" and Structural Transformation

The investment strategy for 2026 no longer revolves around the traditional business cycle but is centered on the structural "Mega Forces" (a concept proposed by BlackRock) that surpass quarterly GDP data.

3.1 Artificial Intelligence: From "Hype" to "Physical Reality"

The narrative of artificial intelligence is shifting from software (such as large language models) to hardware and infrastructure ("Physical AI").

· "Capex Super Cycle": J.P. Morgan points out that data center investment accounts for 1.2%-1.3% of U.S. GDP and continues to rise. This is not a transient trend but a substantial expansion of steel, concrete, and silicon-based technology.

· "Electrotech Economy": Barclays has introduced the concept of the "Electrotech Economy." The demand for energy by artificial intelligence is limitless. Investments in the grid, renewable energy generation, and utilities are seen as the safest ways to participate in the AI wave. HSBC agrees and recommends shifting portfolios to the utility and industrial sectors, which will "power" this revolution.

· Contrarian Viewpoint (HSBC's Warning): In stark contrast to the market's optimistic consensus, HSBC holds a deep skepticism regarding the financial viability of current AI model leaders. According to its internal analysis, companies like OpenAI may face computing lease costs as high as $18 trillion by 2030, leading to a significant funding gap. HSBC believes that while AI is a reality, the profitability of model creators is questionable. This further supports its recommendation to invest in "tools and equipment" (such as chip manufacturers, utilities) rather than model developers.

3.2 The "New Continuum" of the Private Market

BlackRock's 2026 Outlook is centered on the evolution of the private market. They believe the traditional dichotomy between the "public market" (high liquidity) and "private market" (low liquidity) is outdated.

· Rise of the Continuum: Through structures like "Evergreen," European Long-Term Investment Funds (ELTIFs), and secondary markets, private assets are gradually achieving semi-liquidity. This democratizing trend allows more investors to access the "liquidity premium."

· Private Credit 2.0: BlackRock believes that private credit is evolving from the traditional leveraged buyout model to "Asset-Based Financing (ABF)." This model uses real assets (such as data centers, fiber networks, logistics centers) as collateral, rather than solely relying on enterprise cash flow. They believe this brings about "profound incremental opportunities" for 2026.

3.3 Demographics and Labor Shortages

JPMorgan Chase and BlackRock see demographic shifts as a slow but unstoppable driver.

· Immigration Cliff: JPMorgan Chase predicts that the decline in net migration in the U.S. will be a key growth constraint. This implies that the labor force will continue to be scarce and costly, which will not only underpin wage inflation but also further incentivize companies to invest in automation and AI to replace human labor.

Part Four: Asset Allocation Strategy—The Return of "60/40+" and Alpha

Multiple institutions unanimously agree that 2026 will no longer favor the passive "buy the market" strategy popular in the 2010s. In the new market environment, investors will need to rely on active management, diversify into alternative assets, and focus on "quality."

4.1 Portfolio Construction: "60/40+" Model

JPMorgan Chase and BlackRock have explicitly called for reforming the traditional 60% stock/40% bond portfolio.

· The "+" Component: The two institutions advocate for adopting the "60/40+" model, allocating about 20% of the portfolio to alternative assets (private equity, private credit, real assets). This allocation aims to provide returns unrelated to traditional assets, while reducing the overall portfolio volatility in an environment of increased stock and bond correlation.

4.2 Stock Market: Quality and Rotation

· U.S. Stocks: BlackRock and HSBC are overweight on U.S. stocks, primarily benefiting from the artificial intelligence theme and economic resilience. However, HSBC has recently reduced its allocation to U.S. stocks due to overvaluation. They suggest shifting from "mega-cap tech stocks" to broader beneficiaries (such as the financial and industrial sectors).

· International Value Stocks: JPMorgan Chase believes there are strong investment opportunities in European and Japanese value stocks. These markets are undergoing a "corporate governance revolution" (including share buybacks and increased dividends), and their valuations are at a historical discount compared to the U.S.

· Emerging Markets: Schroders is most bullish on emerging markets. They are betting that a weakening U.S. dollar (contrary to other institutions' forecasts) will unlock the value of emerging market assets.

4.3 Fixed Income: The Revival of Yield

The role of bonds is evolving, no longer solely relying on capital appreciation (betting on rate cuts) but returning to its "yield" essence.

· Credit Quality: Given Allianz's warning of rising corporate default rates, HSBC and Schroders strongly favor Investment Grade (IG) bonds over High Yield (HY) bonds. The risk premium of high yield bonds is considered insufficient to compensate for the upcoming default cycle.

· Duration Allocation: Schroders has an overweight stance on duration (especially UK government bonds), expecting central bank rate cuts to be faster than market expectations. JPMorgan Chase, on the other hand, recommends maintaining "flexibility," trading within ranges rather than making large directional bets.

· CLOs (Collateralized Loan Obligations): Schroders explicitly includes AAA-rated CLOs (Collateralized Loan Obligations) in its model portfolio, believing their yield enhancement and structural safety are superior to cash assets.

4.4 Alternative Assets and Hedge Tools

· Infrastructure: Infrastructure investment is the most confident direction in "real asset" trading. BlackRock refers to it as a "cross-generational opportunity" that not only hedges against inflation but also directly benefits from the wave of artificial intelligence capital expenditure.

· Gold: HSBC and Schroders consider gold a key portfolio hedge tool. Against the backdrop of geopolitical fragmentation and potential inflation volatility, gold is seen as a necessary "tail risk" insurance.

Part Five: Risk Assessment — Shadow of Bankruptcy

While the macroeconomic outlook in the United States appears strong due to fiscal stimulus, credit data reveals a more gloomy picture. Allianz offers a sober reflection on the market's optimism.

5.1 Wave of Bankruptcies

Allianz predicts that the global commercial bankruptcy rate will rise by 6% in 2025 and increase by another 5% in 2026.

· "Lagging Trauma": This growth is attributed to the delayed impact of high interest rates. Companies that locked in low rates in 2020-2021 will face a "maturity wall" in 2026, forcing them to refinance at significantly higher costs.

· "Tech Bubble Burst" Scenario: Allianz explicitly simulates a downside scenario, the burst of the "artificial intelligence bubble." In this scenario, it is expected that the U.S. will see an additional 4,500 bankruptcies, Germany 4,000, and France 1,000.

5.2 Vulnerable Industries

The report highlights several industries particularly susceptible to impact:

· Construction: Highly sensitive to interest rates and labor costs.

· Retail/Discretionary Consumer Goods: Squeezed by "K-shaped" consumption trends, with significantly reduced spending by low-income consumers.

· Automotive Industry: Facing multiple pressures of high capital costs, supply chain restructuring, and trade wars.

This risk assessment further supports a "quality-first" approach in asset allocation. The report warns investors to avoid "zombie" companies that survive solely due to cheap funding.

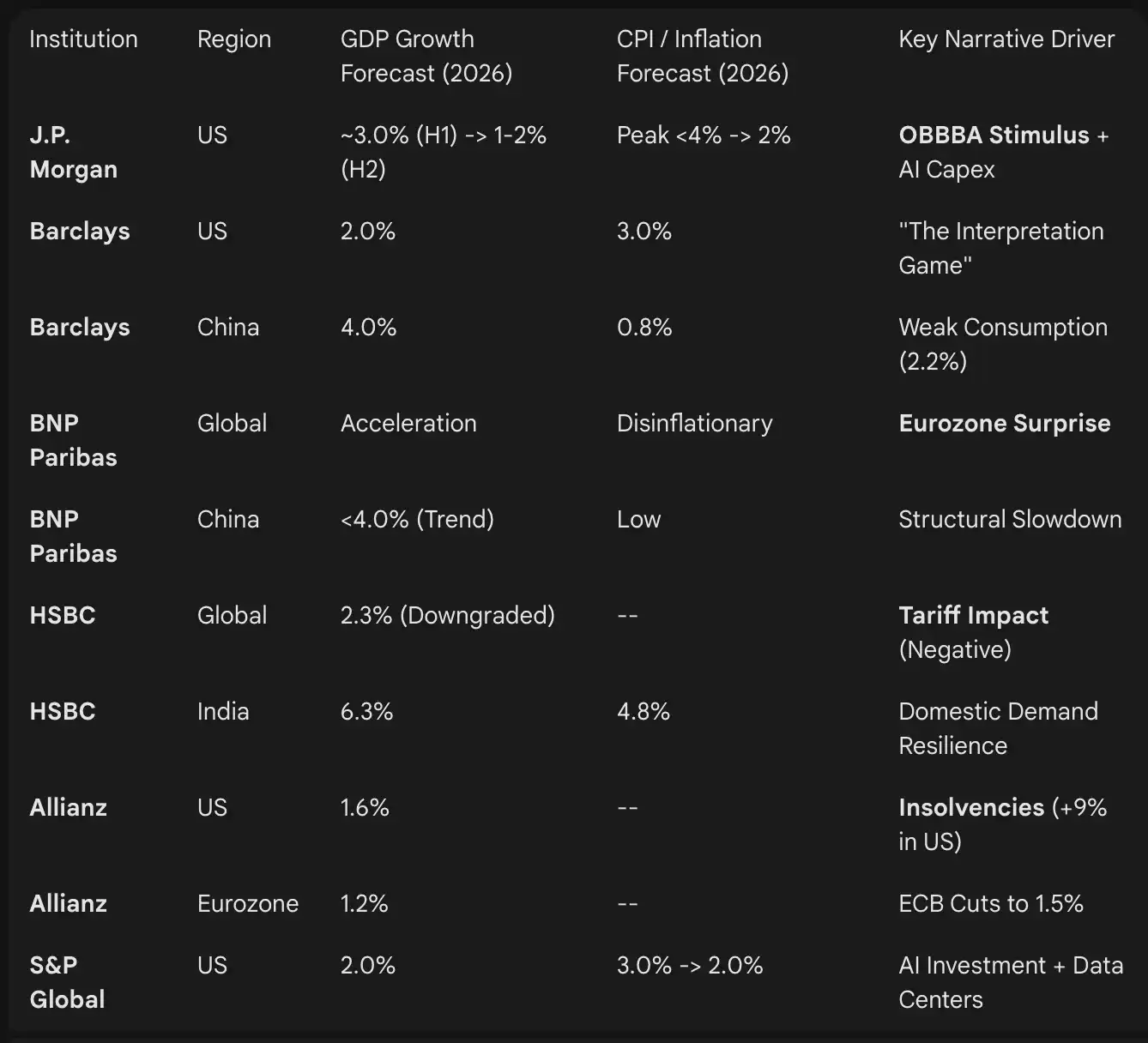

Part 6: Comparative Analysis of Institutional Views

The following table synthesizes the specific GDP and inflation forecasts for 2026 provided in institutional reports, highlighting expected divergences.

Conclusion: Strategic Imperatives for 2026

The investment landscape of 2026 is defined by the tension of two forces: Fiscal and Technological Optimism (U.S. OBBBA plan, Artificial Intelligence) and Credit and Structural Pessimism (Wave of bankruptcies, demographic structural issues).

For professional investors, the path forward requires a departure from broad index-based investments. The characteristics of a "K-shaped" economy - with data center prosperity and construction firm bankruptcies - demand that investors actively make industry selections.

Key Strategic Points:

· Focus on the "OBBBA" Pulse: The timing of the U.S. fiscal stimulus will determine the rhythm of the first half of 2026. Crafting tactical trading strategies for the "stimulus effect" on U.S. assets in the first and second quarters, as well as the potential fallback in the second half, is a prudent move (J.P. Morgan).

· Invest in AI "Tools and Equipment": Avoid valuation risks with purely AI models (HSBC's warning), focus on physical infrastructure such as utilities, grids, and data center REITs (Barclays, BlackRock).

· Achieve Diversification Through the Private Markets: Leveraging the "new continuum" to enter private credit and infrastructure, ensuring these assets are "asset-based" to withstand the impact of a wave of bankruptcies (BlackRock, Allianz).

· Hedge the "Interpretation Game": In a rapidly changing narrative environment, maintain structural hedging tools such as gold and adopt a "barbell strategy" (growth equities + high-quality income assets) to manage volatility (HSBC, Invesco).

2026 will not be a year suited for passive investment but rather one for investors adept at interpreting market signals.

You may also like

Decoding Strategy’s Latest Financial Report: After a $12.4 Billion Loss, How Long Can the Bitcoin Flywheel Keep Spinning?

When earnings reports become electrocardiograms of Bitcoin’s price, Strategy is not merely a company—it’s an experiment testing whether faith can overcome gravity.

Discover How to Participate in Staking

Staking is a digital asset yield product launched by the WEEX platform. By subscribing to Staking products, users can stake their idle digital assets and earn corresponding Staking rewards.

WEEX AI Trading Hackathon Rules & Guidelines

This article explains the rules, requirements, and prize structure for the WEEX AI Trading Hackathon Finals, where finalists compete using AI-driven trading strategies under real market conditions.

From 0 to $1 Million: Five Steps to Outperform the Market Through Wallet Tracking

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

Decoding Strategy’s Latest Financial Report: After a $12.4 Billion Loss, How Long Can the Bitcoin Flywheel Keep Spinning?

When earnings reports become electrocardiograms of Bitcoin’s price, Strategy is not merely a company—it’s an experiment testing whether faith can overcome gravity.

Discover How to Participate in Staking

Staking is a digital asset yield product launched by the WEEX platform. By subscribing to Staking products, users can stake their idle digital assets and earn corresponding Staking rewards.

WEEX AI Trading Hackathon Rules & Guidelines

This article explains the rules, requirements, and prize structure for the WEEX AI Trading Hackathon Finals, where finalists compete using AI-driven trading strategies under real market conditions.