- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

From 'Crime Cycle' to Value Reversion, Outlook on the Four Major Opportunities in the 2026 Cryptocurrency Market

Original Title: Make Revenue, Not Crime | My 2026 Crypto Plan

Original Author: Poopman, Crypto Researcher

Original Translation: Deep Tide TechFlow

Ansem has declared the market's peak, and CT has dubbed this cycle the "Crime Cycle."

Projects with high FDV (Fully Diluted Valuation) and no real-world utility have drained the last penny from the crypto space. Memecoin rug pulls have tarnished the crypto industry's reputation in the public eye.

Even worse, almost no funds are being reinvested back into the ecosystem.

On the other hand, almost all airdrops have turned into "pump and dump" scams. Token Generation Events (TGEs) seem to exist solely to provide early participants and teams with exit liquidity.

HODLers and long-term investors are taking a beating, and most altcoins have never recovered.

The bubble is bursting, token prices are plummeting, and people are furious.

Does this mean it's all over?

Difficult times breed strength.

To be fair, 2025 wasn't a terrible year.

We witnessed the birth of many outstanding projects. Projects like Hyperliquid, MetaDAO, Pump.fun, Pendle, and FomoApp have all demonstrated that there are still true builders in this space striving to drive development in the right way.

This was a necessary "purge" to rid the space of bad actors.

We are reflecting and will continue to improve.

Now, to attract more capital inflow and users, we need to showcase more real-world utility, genuine business models, and revenue streams that can bring actual value to tokens. I believe this is the direction the industry should move toward in 2026.

2025: The Year of Stablecoins, PerpDex, and DAT

Maturing of Stablecoins

In July 2025, the Genius Act was officially signed, marking the birth of the first regulatory framework for payment stablecoins, requiring stablecoins to be backed by 100% cash or short-term government securities.

Since then, Traditional Finance (TradFi) has shown increasing interest in the stablecoin space, with stablecoin net inflows exceeding $100 billion just this year, making it the strongest year in stablecoin history.

RWA.xyz

Institutions have shown a strong preference for stablecoins, believing in their significant potential to replace traditional payment systems, citing reasons such as:

· Lower cost and more efficient cross-border transactions

· Instant settlement

· Low transaction fees

· 24/7 availability

· Hedging against local currency volatility

· On-chain transparency

We have witnessed major acquisition moves by tech giants (such as Stripe acquiring Bridge and Privy), Circle's IPO being oversubscribed, and several top banks collectively expressing interest in launching their own stablecoins.

All these indicate that over the past year, stablecoins have indeed been maturing.

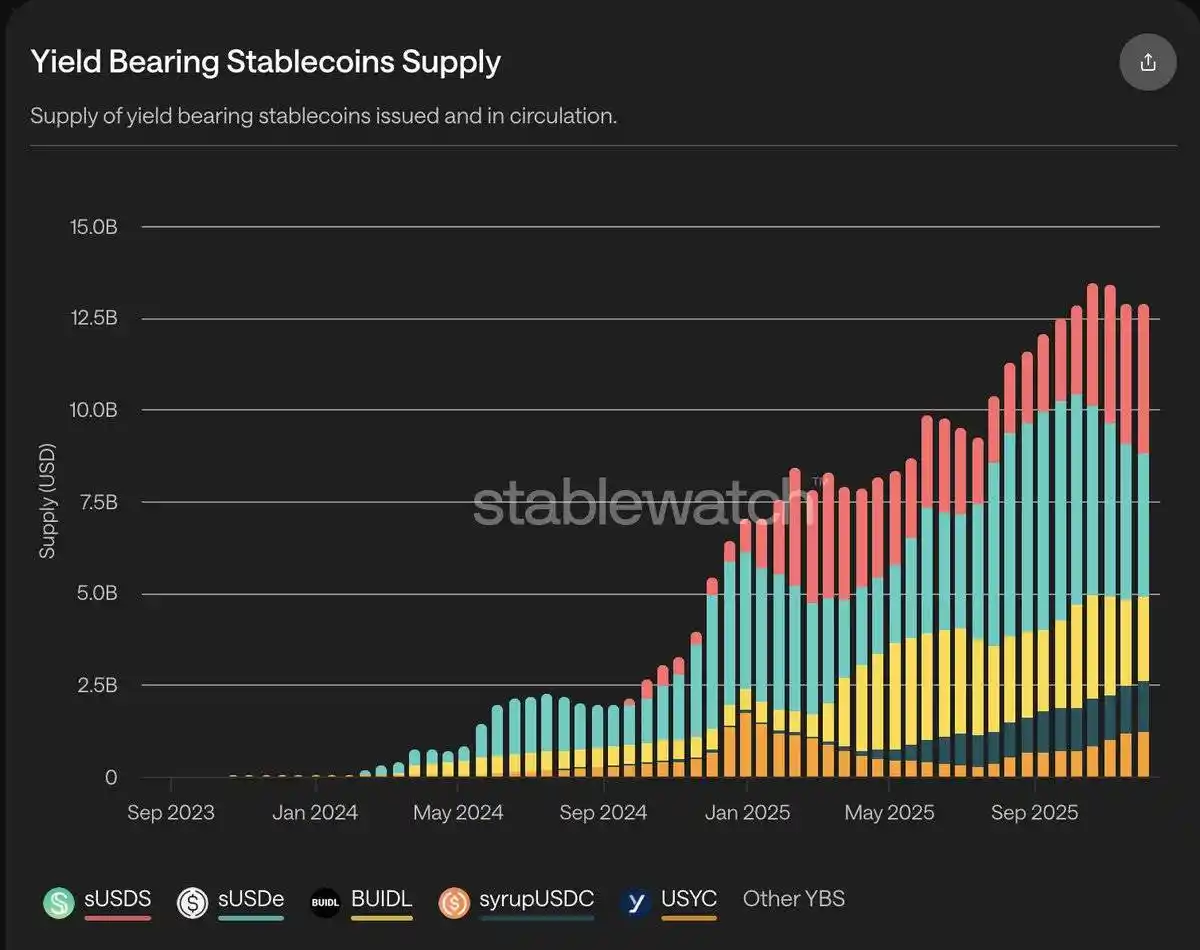

Stablewatch

In addition to payments, another major use case for stablecoins is earning permissionless yield, which we refer to as Yield Bearing Stablecoins (YBS).

This year, the total supply of YBS has actually doubled, reaching $12.5 billion, driven mainly by yield providers like BlackRock BUIDL, Ethena, and sUSDs.

Despite the rapid growth, recent events like the Stream Finance incident and the overall poor performance of the crypto market have impacted market sentiment and reduced the yields of these products.

However, stablecoins remain one of the few truly sustainable and growing businesses in the crypto space.

PerpDex (Decentralized Perpetual Contract Exchange):

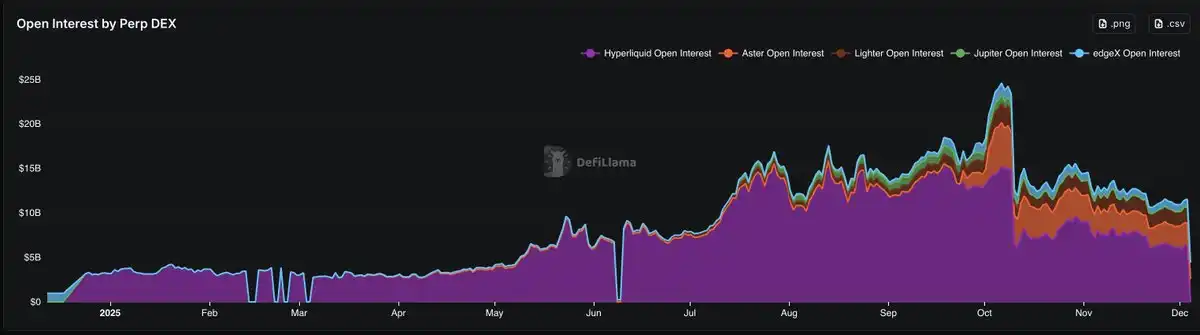

PerpDex is another star of this year.

According to DeFiLlama data, PerpDex's open interest has grown on average 3–4x, increasing from $30 billion to $110 billion, peaking at $230 billion at one point.

The trading volume of perpetual contracts has also seen significant growth, skyrocketing 4x since the beginning of the year, rising from an impressive $800 billion in weekly trading volume to over $3 trillion in weekly trading volume (part of the growth also benefited from incentivized mining), becoming one of the fastest-growing tracks in the crypto space.

However, since the market's significant pullback on October 10 and subsequent market downturn, both of these metrics have shown signs of slowing down.

PerpDex Open Interest (OI), Data Source: DeFiLlama

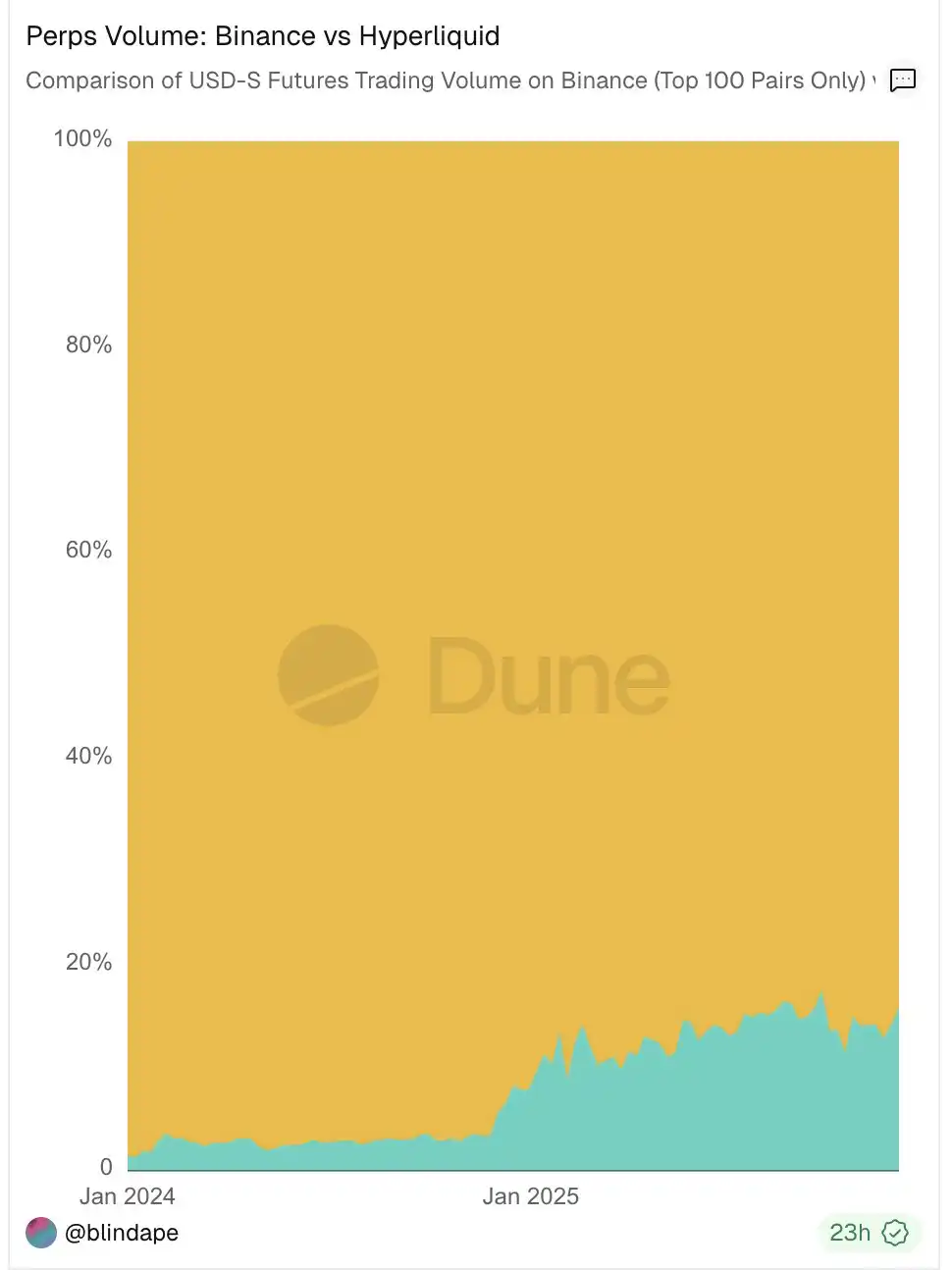

The rapid growth of the decentralized perpetual contract exchange (PerpDex) poses a real threat to centralized exchanges' (CEX) dominant position.

Take Hyperliquid, for example, whose perpetual contract trading volume has reached 10% of Binance's, and this trend is continuing. This is not surprising, as traders can find some advantages on PerpDex that CEX perpetual contracts cannot provide

1. No KYC (Know Your Customer)

2. Decent liquidity, sometimes even comparable to CEX

3. Airdrop speculation opportunities

The valuation game is another key point.

Hyperliquid has demonstrated that decentralized perpetual contract exchanges (PerpDex) can reach extremely high valuation ceilings, attracting a wave of new competitors to enter the arena.

Some new competitors have received backing from large venture capital (VC) firms or centralized exchanges (CEX) (such as Lighter, Aster, etc.), while others are attempting differentiation through native mobile apps, loss compensation mechanisms (such as Egdex, Variational, etc.).

Retail investors had high expectations for these projects at launch in terms of high FDV (Fully Diluted Valuation) and also looked forward to airdrop rewards, leading to the "Points War" phenomenon we see today.

While perpetual decentralized exchanges can achieve high profitability, Hyperliquid has chosen to reinfuse profits back into the token through an "Assistance Fund" buyback of $HYPE (with a buyback amount cumulatively reaching 3.6% of total supply).

This buyback mechanism, by providing real value backflow, has become a key driver of the token's success and has effectively pioneered the trend of the "Buyback Metaverse," prompting investors to demand stronger value anchoring rather than governance tokens with high FDV but no practical use.

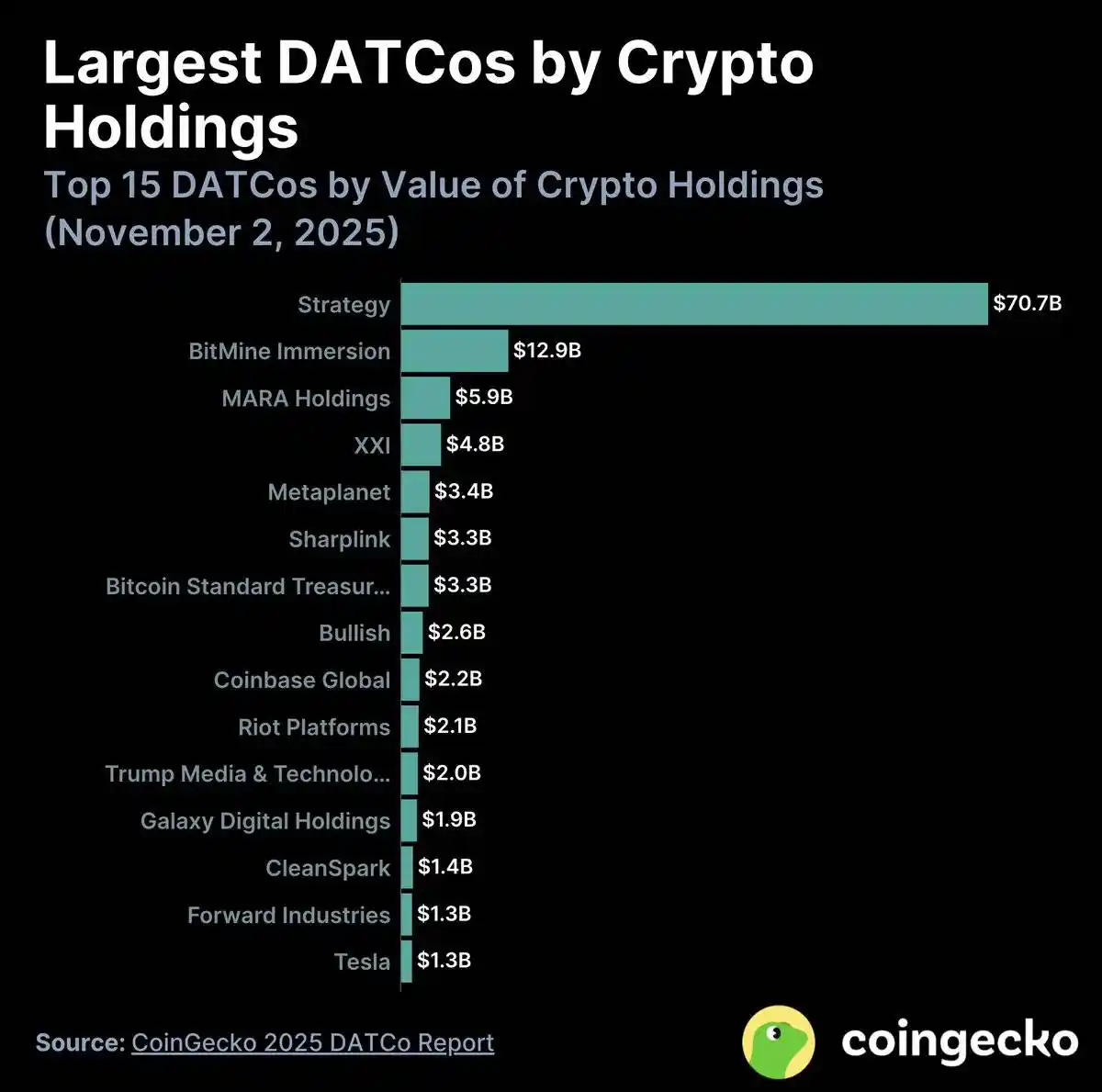

DAT (Digital Asset Treasury):

Due to Trump's pro-crypto stance, we have seen a significant influx of institutional and Wall Street funds into the crypto space.

The inspiration behind DAT comes from MicroStrategy's strategy and has become one of the primary ways for Traditional Finance (TradFi) to indirectly access crypto assets.

In the past year, approximately 76 new DATs have been added. Currently, DAT treasuries collectively hold $137 billion worth of crypto assets. Of these, over 82% are Bitcoin (BTC), about 13% are Ethereum (ETH), and the remainder is distributed among various altcoins.

Refer to the chart below:

Bitmine (BMNR)

Tom Lee's Bitmine (BMNR) emerged as a prominent highlight in this DAT trend and became the largest ETH buyer among all DAT participants.

However, despite early hype, most DAT stocks experienced a "pump and dump" scenario within the first 10 days. Since October 10th, the funds flowing into DAT have plummeted by 90% from July levels, and the majority of DATs' Net Asset Value (mNAV) has fallen below 1, indicating the premium has disappeared, effectively signaling the end of the DAT fever.

Throughout this cycle, we have learned the following:

· Blockchain needs more real-world applications.

· The primary use case in the crypto space is still transactions, yields, and payments.

· Today, people are more inclined to choose protocols with fee-generation potential rather than just decentralization (Source: @EbisuEthan).

· Most tokens need stronger value anchors, tied to protocol fundamentals, to protect and reward long-term holders.

· A more mature regulatory and legislative environment will provide greater confidence for builders and talent to join the space.

· Information has become a tradable asset on the internet (Source: PM, Kaito).

· New Layer 1/Layer 2 projects without a clear positioning or competitive advantage will gradually be eliminated.

So, what's next?

2026: The Year of Predictive Markets, More Stablecoins, More Mobile DApps, More Tangible Income

I believe that in 2026, the crypto space will evolve in the following four directions:

· Prediction Markets

· More Stablecoin Payment Services

· Increased Adoption of Mobile DApps

· Realization of More Tangible Income

Still About Prediction Markets

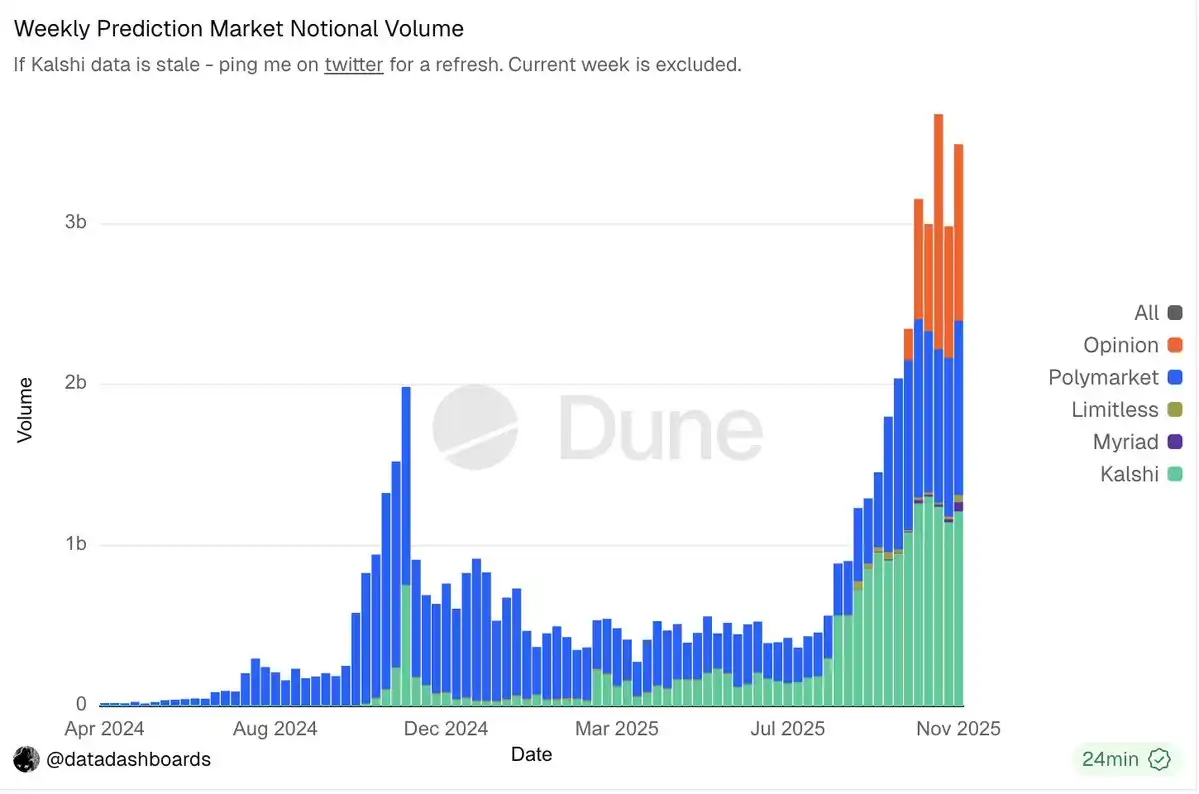

Undoubtedly, prediction markets have become one of the hottest tracks in the crypto space.

「Bet on Anything」

「90% Accuracy in Predicting Real-world Outcomes」

「Participants Bring Their Own Risk」

These headlines have attracted a lot of attention, and the fundamentals of prediction markets are equally compelling.

As of the time of writing this article, the total weekly trading volume of prediction markets has surpassed the peak of the election period (even including total volume then, including wash trading).

Today, giants like Polymarket and Kalshi have completely dominated the distribution channels and liquidity, making it almost impossible for competitors lacking significant differentiation to gain meaningful market share (except Opinion Lab).

Institutions are also starting to pour in, with Polymarket receiving investment from ICE at an $80 billion valuation, and its secondary market valuation reaching $120–150 billion. At the same time, Kalshi completed a Series E funding round at a $110 billion valuation.

This momentum is unstoppable.

Moreover, with the upcoming $POLY token, upcoming IPO, and mainstream distribution channels through platforms like Robinhood and Google Search, the prediction market is likely to become one of the key narratives of 2026.

That being said, the prediction market still has plenty of room for improvement, such as optimizing result resolution and dispute resolution mechanisms, developing methods to combat malicious traffic, and maintaining user engagement over a long feedback cycle, all of which need further enhancement.

In addition to the market's dominant players, we can also expect to see new, more personalized prediction markets, such as @BentoDotFun.

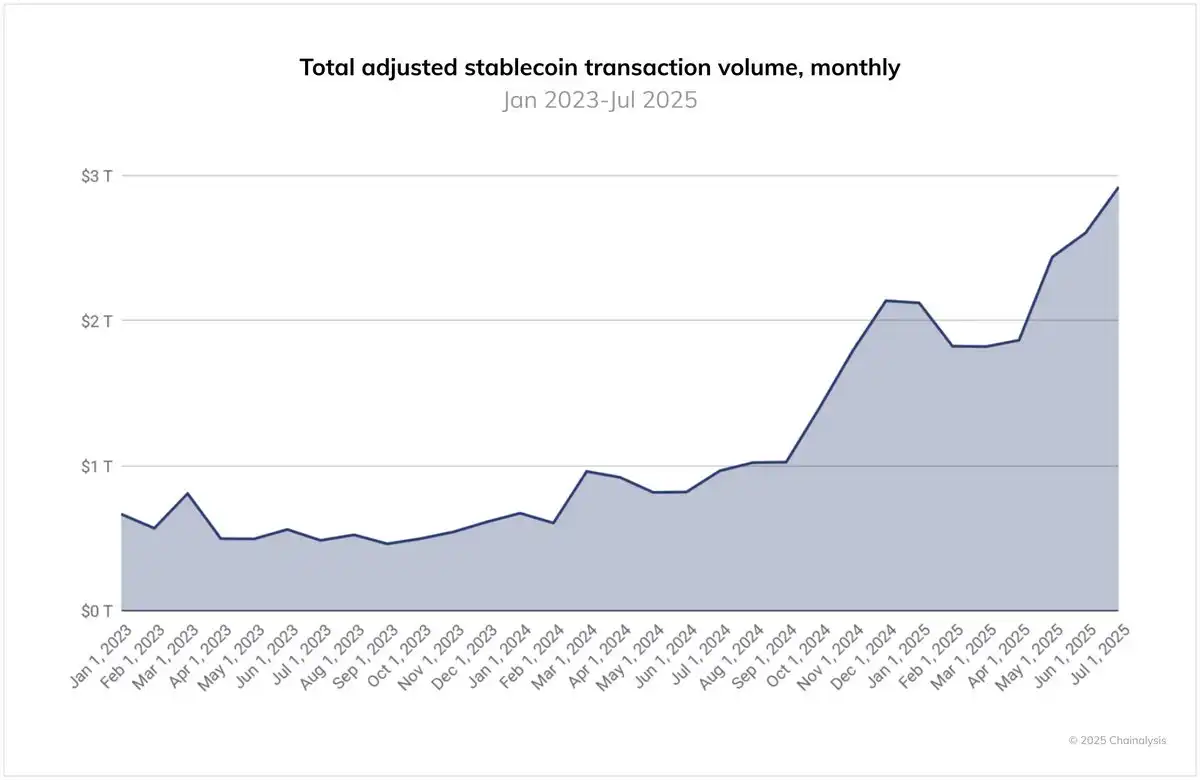

Stablecoin Payments Space

Following the enactment of the "Genius Bill," institutional interest and activity in stablecoin payments have increased, becoming a major driver for its widespread adoption.

Over the past year, the monthly trading volume of stablecoins has risen to nearly $30 trillion, with adoption rates rapidly accelerating. While this may not be a perfect metric, it has already shown a significant increase in stablecoin usage following the enactment of the "Genius Bill" and the European MiCA framework.

On the other hand, Visa, Mastercard, and Stripe are all actively embracing stablecoin payments, whether through supporting stablecoin spending on traditional payment networks or collaborating with centralized exchanges (CEXs) such as Mastercard's partnership with OKX Pay. Today, merchants can choose to accept stablecoin payments, regardless of customer payment methods, demonstrating the confidence and flexibility of Web2 giants in this asset class.

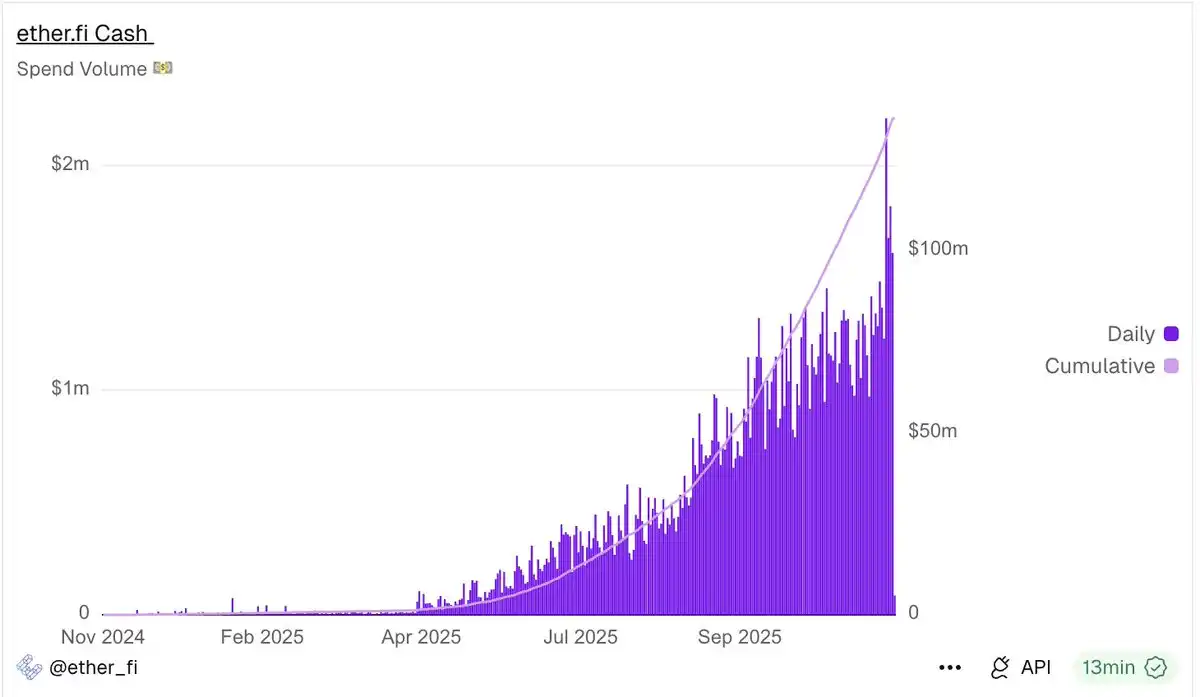

Meanwhile, crypto-native banking services like Etherfi and Argent (now rebranded as Ready) have also started offering card products, allowing users to directly spend stablecoins.

Take Etherfi, for example, whose daily average spending has steadily grown to over $1 million, with no sign of slowing down.

Etherfi

Nevertheless, we cannot overlook some of the challenges that the new crypto-native banks still face, such as high customer acquisition costs (CAC) and the difficulty in earning interest on deposited funds due to users self-custodying their assets.

Some potential solutions include offering in-app token swap functionality or repackaging yield products to sell them as financial services to users.

With payment-focused chains like @tempo and @Plasma gearing up, I anticipate significant growth in the payment sector, especially propelled by the distribution capabilities and brand influence brought by Stripe and Paradigm.

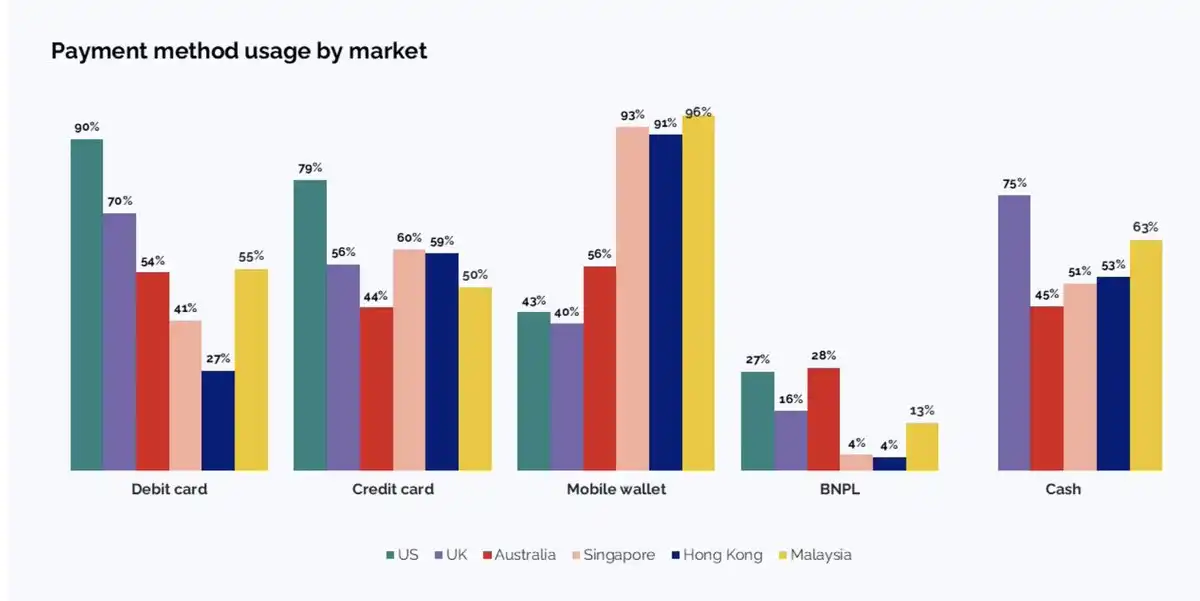

Mobile App Adoption

Smartphones are becoming increasingly ubiquitous globally, with the younger generation driving the shift towards electronic payments.

As of now, nearly 10% of global daily transactions are carried out through mobile devices, with Southeast Asia leading this trend due to its "mobile-first" culture.

Global Payment Method Rankings

This represents a fundamental shift in behavior within traditional payment networks. I believe that as mobile transaction infrastructure has significantly improved compared to several years ago, this shift will naturally extend to the crypto space.

Do you remember account abstraction, unified interfaces, and mobile SDKs in tools like Privy?

Today's mobile user onboarding experience is smoother than it was two years ago.

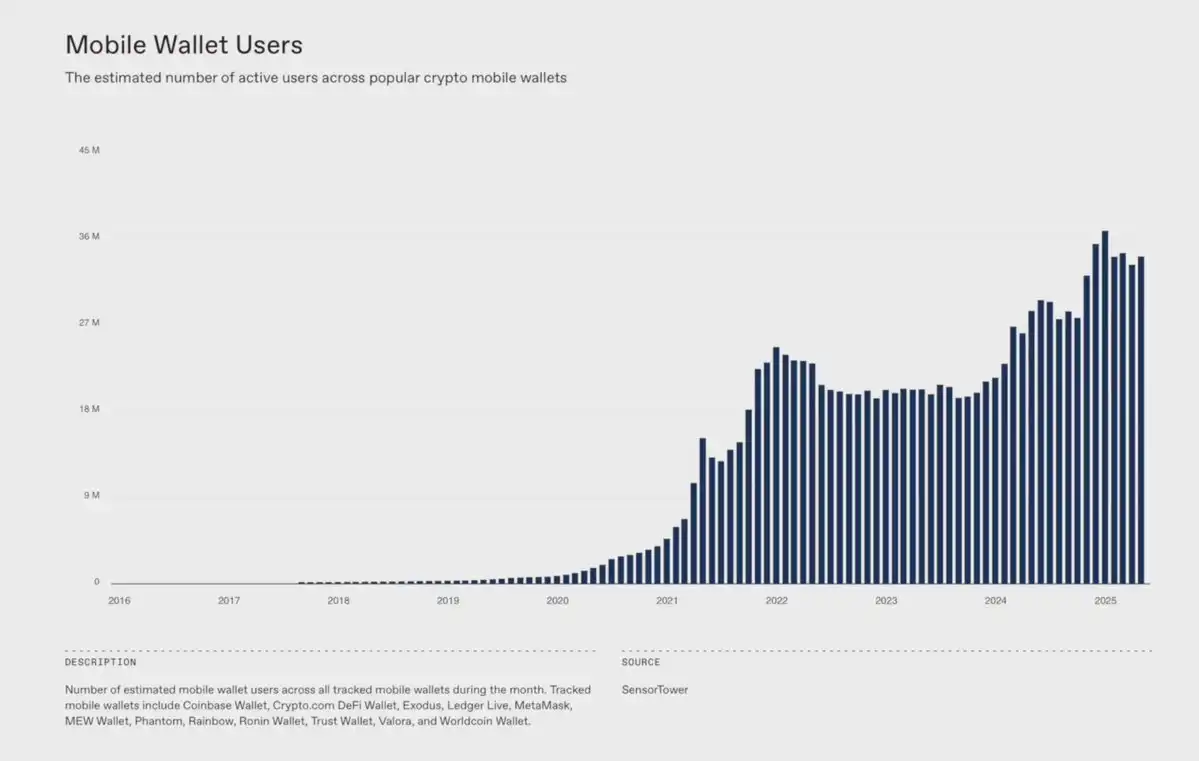

According to a16z Crypto's research, the number of cryptocurrency mobile wallet users has grown by 23% year over year, with no signs of this trend slowing down.

In addition to the evolving consumption habits of Gen Z, we are also seeing a surge in more native mobile dApps by 2025.

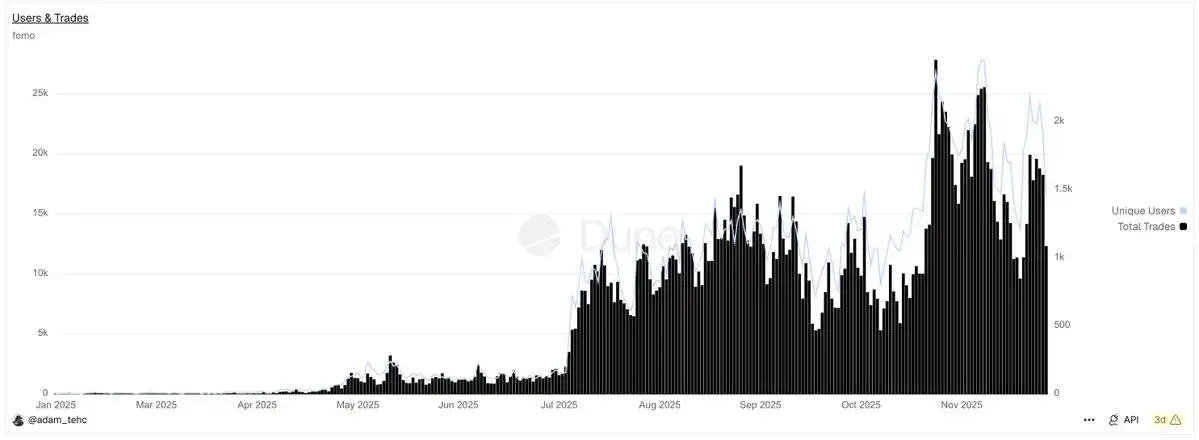

For example, the Fomo App, as a social trading application, has attracted a large number of new users with its intuitive and unified user experience, allowing anyone to easily participate in token trading even without prior knowledge.

Developed in just 6 months, the app achieved a daily average transaction volume of $3 million and peaked at $13 million in October.

With the rise of FOMO, major players like Aave and Polymarket have also started prioritizing mobile-first savings and betting experiences. Meanwhile, newcomers like @sproutfi_xyz are attempting a mobile-first yield model.

As mobile behavior continues to soar, I anticipate mobile dApps to be one of the fastest-growing areas in 2026.

Give Me More Revenue

One of the key reasons people find this cycle hard to believe is simple:

Most tokens listed on major exchanges still generate little to no meaningful revenue, and even when they do, they lack value anchoring to their token or "share." Once the narrative fades, these tokens fail to attract sustainable buyers, often leading to a downward trend.

Evidently, the crypto industry relies too heavily on speculation and lacks focus on real business fundamentals.

Most DeFi projects fall into the trap of designing a "Ponzi scheme" to drive early adoption, but each time, the focus shifts post-Token Generation Event (TGE) to how to offload rather than building a lasting product.

Currently, only 60 protocols have generated over $1 million in revenue in 30 days. In contrast, about 5000–7000 IT companies in Web2 reach this revenue level monthly.

Fortunately, a shift began in 2025 driven by Trump's pro-crypto policies. These policies made profit-sharing possible and helped address the long-standing issue of token value anchoring.

Projects like Hyperliquid, Pump, Uniswap, and Aave proactively focus on product and revenue growth. They recognize that crypto is an ecosystem centered around holding assets, naturally requiring active value flowback.

This is why buyback became such a powerful value anchoring tool in 2025, as it is one of the clearest signals of alignment between the team and investors' interests.

So, which businesses have generated the strongest revenue?

The primary use cases of crypto remain transactions, yield, and payments.

However, due to the cost compression of blockchain infrastructure, on-chain revenue is expected to decline by about 40% this year. In contrast, decentralized exchanges (DEXes), trading platforms, wallets, trading terminals, and applications have emerged as the biggest winners, growing by 113%!

It's time to place more bets on applications and DEXes.

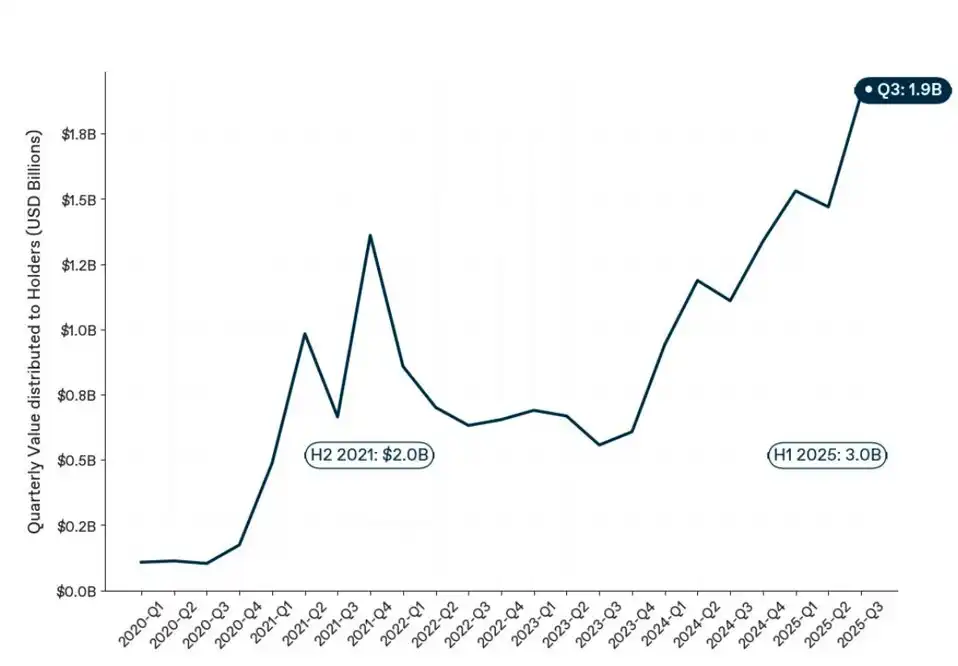

If you still don't believe it, according to 1kx's research, we are actually witnessing the peak of value flowing to token holders in crypto history. Please see the data below:

Summary

The crypto industry is not ending; it is evolving. We are undergoing a market-required "purge," which will make the crypto ecosystem better than ever before, potentially even tenfold.

Projects that can survive, achieve real-world utility, generate actual revenue, and create tokens with practical utility or value capture will ultimately emerge as the biggest winners.

2026 will be a critical year.

You may also like

WEEX AI Trading Hackathon Rules & Guidelines

This article explains the rules, requirements, and prize structure for the WEEX AI Trading Hackathon Finals, where finalists compete using AI-driven trading strategies under real market conditions.

From 0 to $1 Million: Five Steps to Outperform the Market Through Wallet Tracking

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

WEEX AI Trading Hackathon Rules & Guidelines

This article explains the rules, requirements, and prize structure for the WEEX AI Trading Hackathon Finals, where finalists compete using AI-driven trading strategies under real market conditions.

From 0 to $1 Million: Five Steps to Outperform the Market Through Wallet Tracking

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.