- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Five Major Platforms Granted Federal Bank Charters, Crypto Institutions First Time "Included in List"

Original Article Title: "Farewell to the Era of 'Proxy Banks'? Five Cryptocurrency Institutions Get the Key to Direct Access to the Fed's Payment System"

Original Article Author: Ethan, Odaily Planet Daily

On December 12, 2025, the Office of the Comptroller of the Currency (OCC) in Washington, D.C., USA, issued an announcement, conditionally approving Ripple, Circle, Paxos, BitGo, and Fidelity Digital Assets, five digital asset institutions, to transition into federally chartered national trust banks.

This decision did not bring about drastic market fluctuations but was widely seen in the regulatory and financial circles as a watershed moment. Cryptocurrency enterprises that have long operated on the fringes of the traditional financial system and frequently experienced banking service interruptions were, for the first time, officially included in the U.S. federal banking regulatory framework under a "bank" identity.

The change was not sudden but was thorough enough. Ripple plans to establish the "Ripple National Trust Bank," and Circle will operate the "First National Digital Currency Bank." These names themselves already clearly convey the signal released by regulators: digital asset-related businesses are no longer just passively subject to review as "high-risk exceptions" but are now allowed to enter the core of the federal financial system under clear rules.

This shift is starkly contrasted with the regulatory environment of a few years ago. Especially during the banking turmoil of 2023, the cryptocurrency industry was once deeply mired in the so-called "debanking" dilemma, being systematically cut off from the U.S. dollar settlement system. With President Trump signing the "GENIUS Act" in July 2025, stablecoins and related institutions received a clear federal legal status for the first time, providing the institutional premise for OCC's concentrated licensing this time.

This article will focus on four aspects: "What is a Federal Trust Bank," "Why is This License Important," "Regulatory Shift During the Trump Era," and "Response and Challenges for Traditional Finance." It will unravel the institutional logic and real-world impact behind this approval. The core judgment is: the cryptocurrency industry is transitioning from being an "external user" reliant on the banking system to becoming part of the financial infrastructure. This is not only changing the cost structure of payments and settlements but also reshaping the definition of "banking" in the digital economy.

What Is a "Federal Trust Bank"?

To fully understand the significance of this OCC approval, we first need to clarify a commonly misunderstood point: this is not five crypto companies receiving a traditional “banking license” in the conventional sense.

What the OCC has approved is a “National Trust Bank” charter. This is a bank charter type that has long existed in the U.S. banking system but has historically been used primarily for businesses such as trust services and institutional custody. Its core value lies not in “how much business it can conduct,” but in its regulatory oversight and infrastructure status.

What Does a Federal Charter Imply?

Under the dual-track banking system in the U.S., financial institutions can choose to be regulated by either state governments or the federal government. The two are not simply parallel in terms of compliance stringency; there is a clear power hierarchy difference. A federal charter bank license issued by the Office of the Comptroller of the Currency (OCC) means that an institution is directly regulated by the federal treasury system and enjoys “federal preemption,” eliminating the need to individually adapt to the regulatory rules of each state in terms of compliance and operations.

The legal basis for this dates back to the National Bank Act of 1864. Over the following century and a half, this system has been a key institutional tool for the U.S. to create a unified financial market. This is especially critical for crypto companies.

Prior to this approval, whether it was Circle, Ripple, or Paxos, to operate compliantly nationwide in the U.S., they had to apply for Money Transmitter Licenses (MTL) in 50 states, facing a “puzzle-like” system with regulatory stances, compliance requirements, and enforcement scales that were completely different. This was not only costly but also severely restricted business expansion efficiency.

By becoming a federal trust bank, the regulator shifts from individual state financial regulators to the OCC. For the companies, this means a unified compliance path, a national business pass, and a structural enhancement of regulatory credibility.

Trust Banks Are Not “Small-Scale Commercial Banks”

It is important to emphasize that a federal trust bank is not equivalent to a “full-service commercial bank.” The five institutions approved this time are not allowed to attract FDIC-insured public deposits or issue commercial loans. This is also one of the core reasons why traditional banking industry groups (such as the Bank Policy Institute) have questioned this policy, as they see it as “inequitable rights and obligations” in terms of access.

However, from the perspective of the crypto companies’ own business structures, these restrictions are actually highly aligned. Taking stablecoin issuers as an example, whether it’s Circle’s ref="/wiki/article/usd-coin-usdc-269">USDC or Ripple’s RLUSD, their business logic is built on a foundation of 100% reserve asset backing. Stablecoins do not engage in credit expansion, nor do they rely on a fractional reserve lending model, so there is no systemic risk posed by the “maturity mismatch” between deposits and loans that traditional banks face. Under these circumstances, introducing FDIC deposit insurance is not only unnecessary but would also significantly increase compliance burdens.

More importantly, the core of a Trust Bank charter lies in fiduciary responsibility. This means that a licensed institution must legally separate client assets from its own funds and prioritize client interests. This point, especially after the FTX misappropriation of client assets event, holds great practical significance for the entire crypto industry, where asset segregation is no longer a company promise but a mandatory obligation under federal law.

From "Custodian" to "Settlement Node"

Another profound implication of this transformation is that regulatory agencies have undergone a crucial shift in interpreting the scope of a "Trust Bank" business. OCC Chief Jonathan Gould has explicitly stated that the new federal banking charter "provides consumers with new products, services, and credit sources, and ensures that the banking system remains vibrant, competitive, and diverse." This has laid the policy groundwork for embracing crypto institutions.

Within this framework, the transition from state-chartered trust to federal trust for Paxos and BitGo carries strategic value far beyond a mere name change. The crux lies in the fact that the OCC regime grants federal trust banks a crucial right: the eligibility to apply for access to the Fed's payment systems. Therefore, their true aim is not the title of "bank" but the contention for a direct gateway to the central bank's core settlement system.

Take Paxos, for example. While it had already set a compliance benchmark under the strict oversight of the New York State Department of Financial Services, a state charter inherently had its limitations: it could not directly integrate into the federal payment network. The OCC's approval document makes it clear that the new entity post-conversion can continue to engage in stablecoin, asset tokenization, and digital asset custody businesses. This essentially signifies a formal recognition at the institutional level that stablecoins and asset tokenization issuance have become legitimate "banking activities." This is not just a breakthrough for individual companies but a substantive expansion of the scope of "banking" functions.

Once implemented, these institutions are poised to directly connect to central bank payment systems such as Fedwire or CHIPS, no longer needing to rely on traditional commercial banks as intermediaries. Transitioning from a "asset custodian manager" to a "direct node in the payment network" is the most structurally meaningful breakthrough in this regulatory shift.

The Invaluable Nature of This Charter

The true worth of a federal trust bank charter does not lie in the "bank" identity itself but in the possibility that it may have opened a door to a direct pathway to the Federal Reserve's clearing system.

This is also why Ripple CEO Brad Garlinghouse referred to this approval as a "huge step forward," while the Bank Policy Institute (BPI) appeared very uneasy. For the former, this is an improvement in efficiency and certainty; for the latter, it signifies a redistribution of the long-standing monopoly on financial infrastructure.

Direct Access to the Federal Reserve – What Does It Mean?

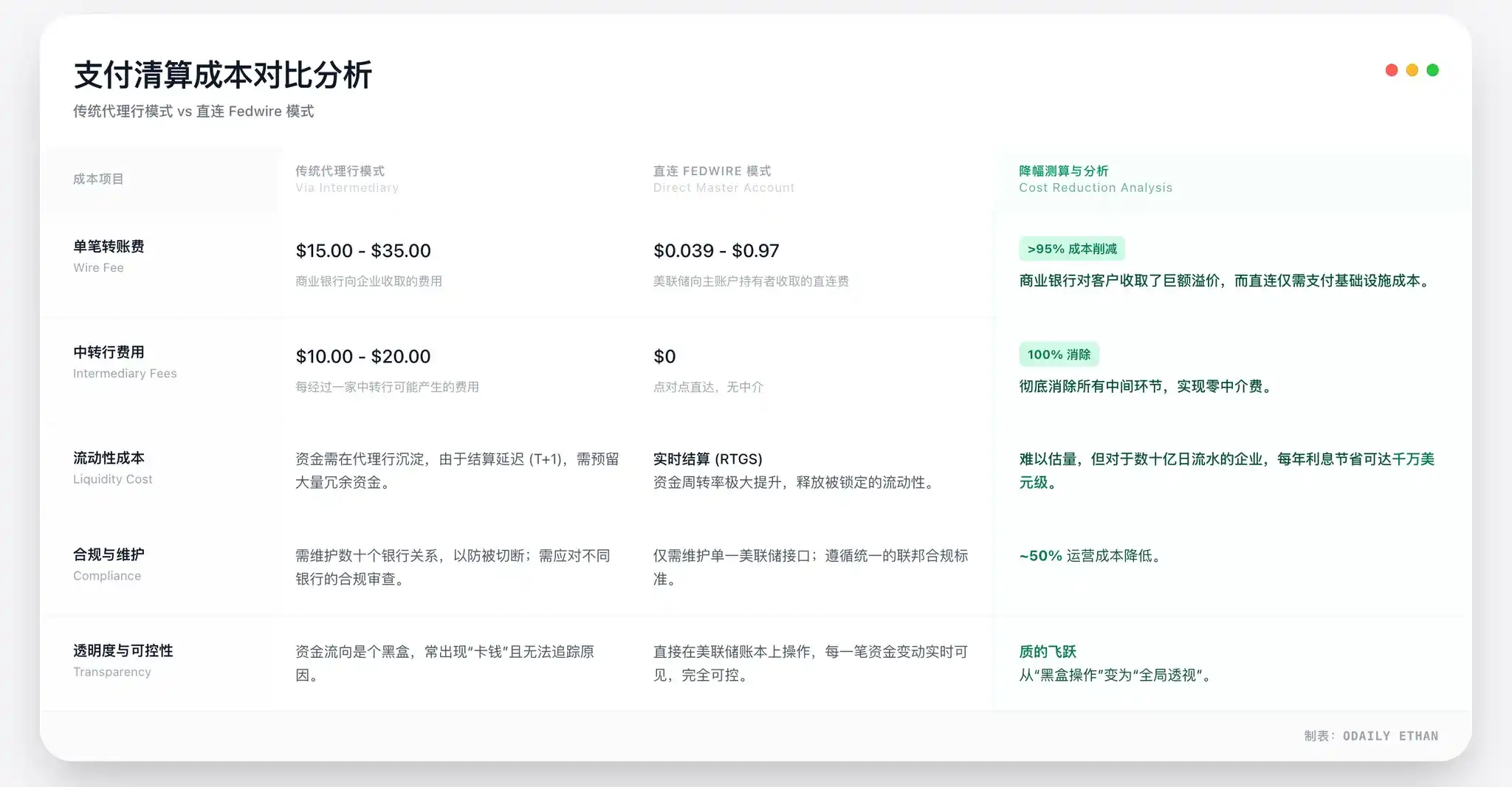

Prior to this, crypto companies have always operated at the "periphery" of the dollar system. Whether it's Circle issuing USDC or Ripple providing cross-border payment services, whenever there is a final settlement involving the dollar, it must be completed through a commercial bank as an intermediary. This model is known in financial terms as the "correspondent banking system." While it may seem like just a longer process on the surface, it has actually brought about three long-standing industry issues.

First is the uncertainty of survival rights. Over the past few years, the crypto industry has faced multiple instances of banks unilaterally terminating services. Once the correspondent bank exits, the fiat channels of crypto companies are cut off in a very short period, stalling their operations. This is what the industry calls the "de-risking" risk.

Second is the cost and efficiency issue. The correspondent banking model means that every fund transfer must go through multiple layers of bank clearing, each layer accompanied by fees and time delays. For high-frequency payments and stablecoin settlements, this structure is inherently unfriendly.

Third is the settlement risk. The traditional banking system generally operates on a T+1 or T+2 settlement cycle, where funds are not only tied up in transit but also exposed to bank credit risks. When Silicon Valley Bank collapsed in 2023, Circle had around $3.3 billion USDC reserves temporarily stuck in the banking system, an event that is still seen as a warning case for the industry.

The change brought about by obtaining a Federal Reserve bank identity is precisely in this structure. At the institutional level, licensed entities have the eligibility to apply for a "master account" with the Federal Reserve. Once approved, they can directly access federal-level clearing networks like Fedwire, completing real-time, irrevocable final settlement within the dollar system without relying on any commercial bank intermediaries.

This means that in the crucial fund settlement stage, institutions like Circle and Ripple are, for the first time, standing on the same "system-level" as JPMorgan Chase and Citibank.

Ultimate Cost Advantage, Not Marginal Optimization

The cost reduction obtained by having a master account is structural, not marginal. The core principle is that a direct connection to the Federal Reserve payment systems (such as Fedwire) completely bypasses the multi-tier intermediation of traditional correspondent banks, thereby eliminating the corresponding intermediary fees and markups.

We can extrapolate based on industry practices and the Fed's 2026 public fee schedule. Calculations show that in high-frequency, high-value scenarios such as stablecoin issuance and institutional payments, this direct connection model can reduce overall settlement costs by approximately 30%-50%. The cost reduction mainly comes from two aspects:

1. Direct Fee Advantage: The Federal Reserve's fee for Fedwire large-value payments is much lower than a commercial bank's wire transfer pricing.

2. Structural Simplification: Various fees related to correspondent banking, account maintenance, and liquidity management are eliminated.

Taking Circle as an example, managing nearly $80 billion in USDC reserves faces significant daily fund flows. If a direct connection is established, with only the payment channel fee to be paid, the annual savings could amount to hundreds of millions of dollars. This is not a marginal optimization but a fundamental cost restructuring at the business model level.

Therefore, the cost advantage gained from having a master account is significant and certain, directly translating into a stablecoin issuer's core moat in fee competition and operational efficiency.

The Legal and Financial Attributes of Stablecoins Are Evolving

When a stablecoin issuer operates as a Federal Trust Bank, the attributes of its product also undergo a transformation. In the old model, USDC or RLUSD were more akin to a "digital token issued by a tech company," with their security highly dependent on the issuer's governance and the robustness of the partner banks. In the new structure, the stablecoin reserves will be placed in a Trust system under the OCC federal regulatory framework, with a legal separation from the issuer's own assets.

This is not equivalent to a Central Bank Digital Currency (CBDC), nor does it have FDIC insurance, but with the combination of "100% full reserves + federal-level regulation + trustee obligations," its credit rating is significantly higher than most offshore stablecoin products.

A more tangible impact is seen at the payment level. Taking Ripple as an example, its On-Demand Liquidity (ODL) product has long been restricted by bank operating hours and fiat channel availability. Once integrated into the federal clearing system, the switching between fiat and on-chain assets will no longer be restricted by time windows, significantly enhancing the continuity and certainty of cross-border settlements.

Market Reaction, Instead More Rational

Although this development has been seen as a milestone within the industry, the market reaction did not show drastic fluctuations. Whether it's XRP or USDC-related assets, the price changes have been relatively limited. However, this does not mean that the value of the license is underestimated; rather, it is more likely to indicate that the market has already viewed it as a long-term institutional change rather than a short-term trading theme.

Ripple CEO Brad Garlinghouse has defined this development as the "gold standard on the stablecoin compliance path." He not only emphasized that RLUSD is now under the dual regulation of the federal (OCC) and state-level (NYDFS), but also directly took a shot at traditional bank lobbying groups: "Your anti-competitive tactics have been exposed. You complain that the crypto industry does not follow the rules, but now we are directly under the OCC's regulatory standard. What are you afraid of?"

At the same time, Circle also pointed out in a related statement that the national trust bank charter will fundamentally reshape institutional trust, enabling issuers to provide more trustee-based digital asset custody services to institutional clients.

Both parties' statements converge: From "being served by banks" to "becoming part of the banks," crypto finance is entering a whole new stage. The federal trust bank charter is not just a license but also a secure pathway into the crypto market for institutional capital that has been waiting on the sidelines due to compliance uncertainty.

The "Golden Age" of the Trump Era and the "GENIUS Act"

If we turn back time three to four years, it would be hard to imagine that crypto companies could be federally recognized as "banks" by the end of 2025. The catalyst for this transformation was not a technological breakthrough but a fundamental shift in the political and regulatory environment.

The return of the Trump administration and the implementation of the "GENIUS Act" together paved the way for crypto finance to access the federal system.

From "Debanking" to Institutional Acceptance

During the Biden administration, the crypto industry was in a prolonged period of strong regulation and high uncertainty. Especially after the FTX collapse in 2022, the regulatory tone shifted to "risk isolation," requiring the banking system to stay away from crypto businesses.

This phase was internally referred to as "debanking" by the industry and was also described by some lawmakers as "Operation Choke Point 2.0." According to a subsequent investigation by the House Financial Services Committee, several banks, under informal regulatory pressure, severed ties with crypto companies. The successive exits of Silvergate Bank and Signature Bank were the prominent manifestations of this trend.

The regulatory logic at that time was very clear: rather than laboriously regulating the cryptographic risk, it was better to isolate it outside the banking system.

This logic underwent a fundamental reversal in 2025.

During the election campaign, Trump publicly supported the cryptocurrency industry multiple times, emphasizing making the U.S. the "global cryptocurrency innovation center." Upon reassuming office, cryptocurrency assets were no longer simply seen as a source of risk but were included in a more macroscopic financial and strategic consideration.

The key shift was that stablecoins began to be seen as a tool extending the dollar system. On the day the "GENIUS Act" was signed, the White House clarification explicitly stated that regulated USD stablecoins help expand U.S. debt demand and consolidate the U.S. dollar's international status in the digital age. This essentially redefined the role of stablecoin issuers in the U.S. financial system.

Institutional Role of the "GENIUS Act"

In July 2025, Trump signed the "GENIUS Act." The significance of this act lies in establishing a clear legal identity for stablecoins and related institutions at the federal level for the first time. The act explicitly allows non-bank institutions to, after meeting certain conditions, operate as "qualified payment stablecoin issuers" subject to federal regulation. This provided companies like Circle and Paxos, which were originally outside the banking system, with a systemic entry point into the federal framework.

More importantly, the act imposed a stringent requirement on reserve assets: stablecoins must be 100% fully backed by U.S. dollars or highly liquid assets like short-term U.S. Treasuries. This essentially excluded the space for algorithmic stablecoins and high-risk allocations and closely aligned with the trust banking model of "no lending, no investment."

Additionally, the act established priority of redemption for stablecoin holders. Even in the event of the issuer's bankruptcy, the related reserve assets must be used first to redeem the stablecoins. This provision significantly reduced regulatory concerns about "moral hazard" and enhanced the credibility of stablecoins at the institutional level.

Within this framework, the OCC issuing federal trust bank charters to cryptocurrency companies naturally became a compliant institutional implementation.

Defense of Traditional Finance and Future Challenges

For the cryptocurrency industry, this was a belated institutional breakthrough; however, for Wall Street incumbents, it was more like a territory invasion that must be countered. The OCC's approval of five cryptocurrency firms to transition to federal trust banks did not receive unanimous applause but rather swiftly triggered fierce defense from the traditional banking sector alliance, represented by the Bank Policy Institute (BPI). The war between "new and old banks" has only just begun.

The BPI's Fierce Counterattack: Three Key Allegations

The BPI represents the interests of giants such as JPMorgan Chase, Bank of America, and Citigroup. Immediately after the OCC announced its decision, its senior management raised sharp questions, with the core argument pointing directly at a deep-seated conflict in regulatory philosophy.

First is the issue of "Wolves in Sheep's Clothing" through regulatory arbitrage. The BPI points out that these crypto institutions applying for a "trust" charter are actually engaging in banking core functions such as payments and clearing, with a systemically important role even surpassing that of many mid-sized commercial banks.

However, through the trust charter, their parent companies (such as Circle Internet Financial) cleverly sidestep the Fed's consolidated supervision required of a "bank holding company." This means regulators have no authority to review the parent company's software development or external investments — if a code vulnerability in the parent company leads to bank asset losses, a significant risk exposure would exist in a regulatory blind spot.

Second is the undermining of the sacred principle of "Separation of Banking and Commerce." The BPI warns that allowing tech companies like Ripple and Circle to own banks essentially breaks down the firewall that prevents corporate giants from using bank funds for corporate welfare. What traditional banks find even more displeasing is the unfair competition: tech companies can leverage their monopolistic advantages in social networks and data flows to push out banks without bearing the Community Reinvestment Act (CRA) obligations that traditional banks must fulfill.

Lastly, there is the concern about systemic risk and the lack of a safety net. Since these new trust banks lack FDIC insurance backing, if there is a panic in the market about stablecoin destabilization, traditional deposit insurance cannot act as a buffer. The BPI argues that this unprotected liquidity run would rapidly spread and evolve into a systemic crisis similar to 2008.

The Fed's "Final Hurdle"

Receiving a charter from the OCC does not mean smooth sailing. For these five newly minted "federal trust banks," the last and most crucial hurdle to access the Federal Reserve's payment system — the authority to open a master account — still squarely rests with the Fed.

Although the OCC has recognized their banking status, in the U.S.'s dual banking system, the Federal Reserve holds independent discretion. Previously, Wyoming's crypto bank, Custodia Bank, initiated a lengthy lawsuit after being denied a master account by the Fed, indicating that between obtaining a charter and true access to Fedwire, there still exists a significant gap.

This is also the next main battlefield of the traditional banking industry (BPI) lobbying. Since they cannot stop the OCC from issuing charters, the traditional banking forces will inevitably pressure the Federal Reserve to set a very high threshold for approving primary accounts—such as requiring these institutions to prove their anti-money laundering (AML) capabilities are on par with universal banks like JPMorgan Chase, or requiring their parent companies to provide additional capital backing.

For Ripple and Circle, this game is just entering the second half: if they obtain a license but cannot open a primary account with the Federal Reserve, they will still only be able to operate through an agency model. The prestige of being a "national bank" will be greatly diminished.

Conclusion: The Future, More Than Just Regulatory Games

It can be anticipated that in the future, this game revolving around crypto banking will obviously not stay at the licensing level.

On the one hand, the attitude of state regulatory agencies still remains uncertain. Strong state regulators such as the New York State Department of Financial Services (NYDFS) have long played a leading role in crypto regulation. As federal preemption expands, whether state regulatory authority is weakened may trigger new legal disputes.

On the other hand, although the "GENIUS Act" has already taken effect, many detailed implementation rules still need to be formulated by regulatory agencies. Specific rules such as capital requirements, risk isolation, and cybersecurity standards will be the policy focus for the foreseeable future. The game among different stakeholders is likely to unfold in these technical terms.

Furthermore, changes at the market level are also worth noting. As crypto institutions gain banking status, they may become both partners for traditional financial institutions and potential acquisition targets. Whether traditional banks acquire crypto institutions to complement their technological capabilities, or crypto companies enter the banking industry in reverse, the financial landscape could undergo structural adjustments as a result.

What is certain is that this OCC approval is not the end of the controversy, but a new beginning. Crypto finance has entered the institutional mainstream, but how to find a balance between innovation, stability, and competition will still be the question that U.S. financial regulation must answer in the coming years.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.